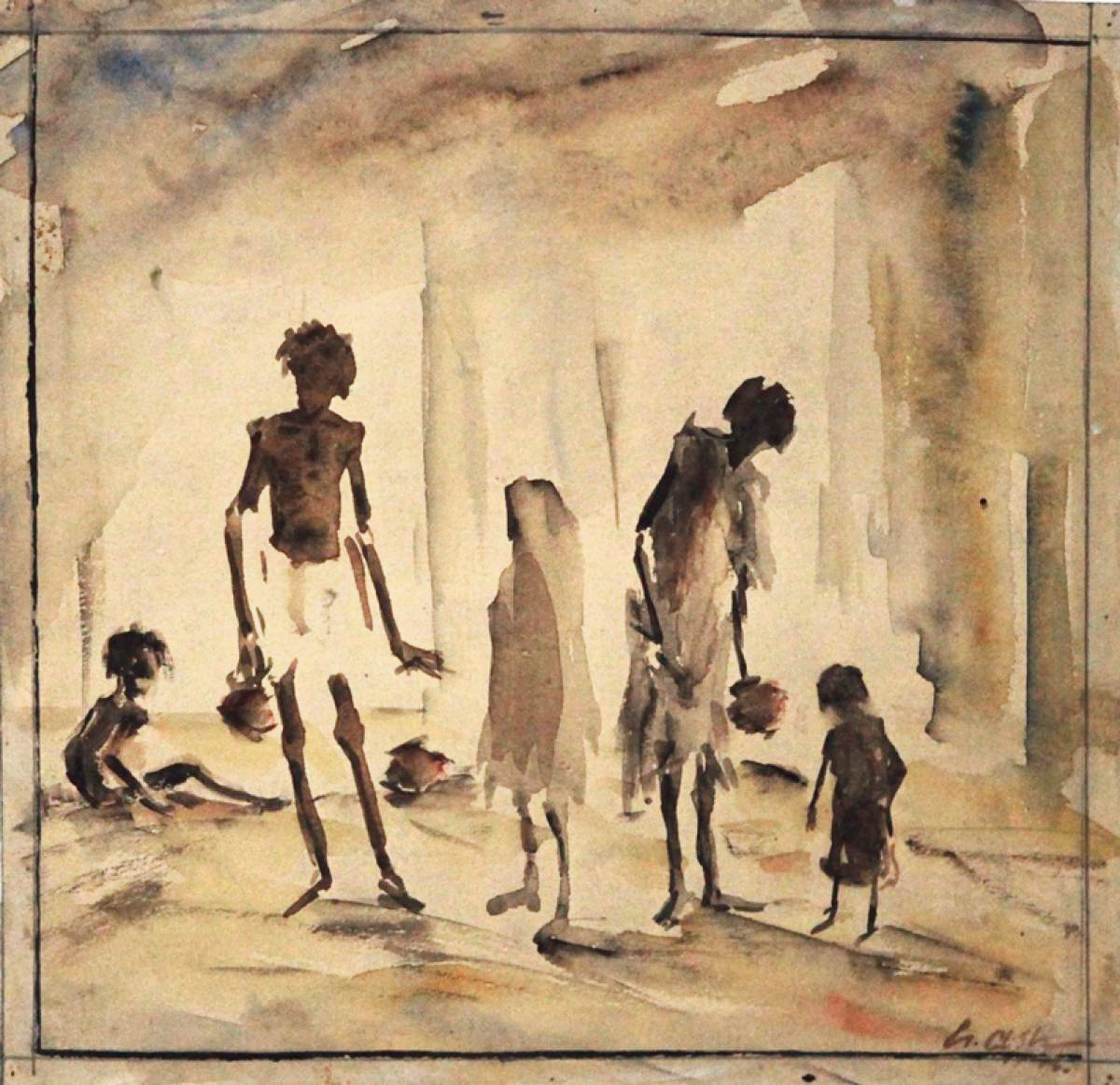

Why does capitalism produce hunger despite the overproduction of goods? Nathan Eisenberg delves into the contours of the global food system, its political economy, and its contradictions in the first of a series of articles.

Hungry child,

I didn’t make this world for you.

You didn’t take any stock in my railroad.

You didn’t invest in my corporation.

Where are your shares in standard oil?

I made this world for the rich

And the will-be-rich

And the always-have-been-rich.

Not for you,

Hungry child.

Langston Hughes, “God to Hungry Child”

The coronavirus pandemic has precipitated an uneven and multivariate crisis affecting every country. This has made a number of severe and contradictory impacts on the global food system, revealing its structural vulnerabilities. The system of food production and distribution today is based on interdependent relations that take on the appearance of formally equal market trade in necessities but form the core of the international organization of class relations. Because food production is organized for capital accumulation and not for human consumption needs, it will always be vulnerable to shocks and, as this series of articles will argue, structurally incapable of actually feeding humanity.

The jumping-off point for this investigation will be a methodological note about apprehending the world’s subsistence system as a singular object, a ‘food regime’. Harriet Friedman and Philip McMichael defined the concept of a food regime as a “rule governed structure,”1 a set of “international relations of agricultural production and consumption [linked] to forms of accumulation broadly distinguishing periods of capitalist transformation since 1870,” which constituted a coherent price-governed world market.2 Food regime analysis, fusing the concept of the ‘regime of accumulation’ from the Regulation school3 with insights about the spatial dialectic between center and periphery from World-Systems Analysis, is a framework for attending to the global scale of agricultural production and the contradictions that necessarily emerge from this.

Friedman and McMichael specifically posited that there were two distinct food regimes defining the passage into globalization, both mediated by agricultural capital in the US. First, from 1870 to World War I, there was a ‘colonial-diasporic’ food regime, with two geographic components: monoculture plantations in tropical colonies, and family farming in the temperate settler frontiers of the US, Canada, Argentina, New Zealand, Uruguay and South Africa. The former sites provided sugar-dense fruit and starches, and the latter settler-colonial regions provided a steady flow of cheap wheat, all shipped to the imperial metropole. Together, agricultural production in these peripheries converged to supplement the industrialization of Europe. The second food regime, following an interwar ‘interregnum’ in which no coherent regime stabilized, began in earnest in 1947 with the negotiation of the General Agreement on Tariffs and Trade (GATT) and the Bretton Woods system. This ‘mercantile-industrial’ regime was organized around the export of US agricultural surpluses abroad, often in the form of aid, to the decolonizing periphery as a means of combating communist movements. The canonical family farm experienced its twilight as the US farming sector was substantially concentrated and centralized in terms of both landownership and capital. The resulting postwar agribusiness complex, with the help of philanthropic funds such as the Ford Foundation, began to internationalize through the export of productive capital such as seeds, machinery and chemical inputs.4 This period also inaugurated the channeling of grain surpluses through the ‘animal protein complex’ of cattle, poultry and hogs. In the mid-1970s, there were monumental food shortages, coinciding with stagflation and the energy crisis, which precipitated a shift from the state developmentalism of the midcentury towards a world market dominated by transnational firms.5

There is some debate today about whether this constitutes a ‘third food regime,’ perhaps defined by multinational corporations, or landless peasant movements, or the supermarket revolution.6 The literature on food regimes has to some extent become a search for a suitable historical phenomenon with which to anchor the posited ‘ideal-type’ structure.7 Historiographic periodization schemes tend to smuggle in an element of the synchronic, organizing history into internally stable modes or structures that place the explanatory onus onto the discontinuities and transitions between them. By focusing on stable ‘regimes’ such transitions may then appear sudden and inexplicable. However, viewed diachronically and dialectically, the successive food regimes of the 19th and 20th centuries can be seen as contingent arrangements of immanent tendencies in capital accumulation, marked primarily by the centralization and internationalization of capital and the neoliberal encounter of the underdeveloped periphery with surplus capital from the core.

It is less pertinent then to identify the exact concrete formulation with which to characterize the ideal-typical regime that governs today, and which distinguishes it from past periods, than it is to trace the contingent development of these contradictions over the longue durée. As McMichael observed, “the simplification of industrial agriculture that began with colonial monocultures, and has been universalised through successive food regime episodes, has now reached a fundamental crisis point.”8 However it is spatially and ecologically organized, each food regime expresses basic contradictions between the subsistence of the proletariat and the accumulation of the capitalists. The development of these contradictions via the concerted struggle between classes gives rise to cycles through periods of relative stabilization, adequate to neutralize class conflict for a time, and acute destabilization when the latent vulnerabilities pang the empty bellies of large segments of the population. Now, as in many moments in the past, hunger is a necessary outcome of the global food regime.

To understand the history of subsistence, McMichael employs Fernand Braudel’s tripartite layering of social time—the event, the conjuncture, and the longue durée.9 In McMichael’s analysis, the grandest scale, the longue durée, refers to the “rational planning of the planet” in mitigating hunger, but for our purposes might be extended to the entire modern period defined by the metabolic rift of agrarian capitalism.10 This series of articles will be loosely organized according to this historiographic schema. In the second instalment, the fundamental agrarian questions of longue durée as they appeared to political economists, ecologists, historians and communist revolutionaries will be surveyed in depth. The schematic notion of discrete food regimes will be critiqued in favor of a viewpoint which proceeds from developments in the class struggle as mediated by land, food and agrarian production. Stable regimes of food production and distribution will be seen to result from determinate class strategies. In the third instalment, the dynamics of transition between food regimes will be explored via a historical reconstruction of the constitution, disintegration, transition and reconstitution of the imperialist system in the 20th century, arriving at a narrative of discernible conjunctures. In the third instalment, the ecological aspects of the present conjuncture will be laid out. For this first instalment, we will start at the end, beginning with the immediate concrete appearance of the conjuncture as it is glimpsed in the disastrous ‘event’ of the COVID-19 pandemic in the last 20 months. This will proceed in three steps.

First, this article will survey the range of food security emergencies precipitated by or coinciding with COVID-19 and the responses of the humanitarian apparatus. These are proximate flashpoints of local crises, a freak convergence of disasters, coinciding within the evental crisis of the pandemic. The disasters in question span meteorology, pest ecology and civil war. While such instances can be situated within the longue durée of capitalist ecology, this undertaking is beyond the boundaries of the essay, save for some preliminary comments. Instead, they will be approached as external shocks which expose the hidden structure of the conjuncture in all its vulnerabilities. The ultimate goal of this analysis is to situate these flashpoints within the wider context, to peel back the proximate in search of ultimate structural drivers and to go beneath the contingencies to locate the overdetermining circumstances.

To this end, the second section will be a brief conjunctural history of the development of global food commodity chains and the foundation of agricultural production on export trade, roughly following the food crisis of 1972–1974 and identifying something of a food regime logic in the brittle reconstitution of social reproduction undertaken in the period. This reconstitution takes place through the dialectical movements of the law of value, as agricultural capital is concentrated and agricultural production globalized. In the final section, the human cost of the rationalization and subsumption of farming will be examined alongside the pattern of global deindustrialization, leading to a remainder of ‘surplus populations’ experiencing social dis-integration in the foreclosure of the ‘modernization’ development paradigm. There will be an exploration into the way these economic arrangements are specifically vulnerable to disruption from the pandemic, as the dominant conditions within the conjuncture translate into an evental crisis, leading to the largest scale increase in starvation seen in a generation.

1) Plagues

Four days before the release of its annual Global Report on Food Crises (GRFC)11 in April 2020, the Global Network Against Food Crises (GNAFC) was forced to issue preemptive revisions to findings already made obsolete by the emerging coronavirus pandemic. The GRFC’s global estimate of the number of people facing severe food insecurity, based on data collected in 2019, was calculated to be an already record-breaking 135 million people in the 55 most food-insecure countries,12 with 32% of that population concentrated in Yemen, Afghanistan and the Democratic Republic of Congo (DRC).13 Based on expectations of disruptions to food imports, the impact of lost income on ‘purchasing power,’ huge swings in prices, and increased conflict and displacement caused by the pandemic, the UN World Food Programme (WFP) preempted the outdated report with a revised prediction that as many as 265 million people14 would be vulnerable to acute food insecurity by the end of 2020 unless urgent action was taken. The most recent estimate, as of November 2021, maintains that 283 million people in 80 countries are acutely food insecure or at high risk.15

This debacle prompts two distinct questions we can ask about the food crisis: In what kind of system would starvation reach such proportions? And, what systemic vulnerabilities exist such that the pandemic would nearly double the number of the starving masses in a matter of months? Such a proliferation of emergencies would promise to overwhelm any humanitarian infrastructure in place, overturn years of development and result in unmitigated democide at a scale dwarfing the pandemic itself. As the WFP chief economist Arif Husain put it, “The scenario in poor countries is too gruesome to comprehend.”16

This alarming scenario prompted the World Food Programme to activate a global Level 3 (L3) emergency designation for the first time in its history on March 30, 2020.17 Regional L3 protocols occur when existing regional capacities are overwhelmed and resources need to be redistributed from other WFP country offices to the most dire frontlines. A “global” L3 requires the entire organization to be reoriented and retooled to meet the explosion of need across regions.18

In April, as existing humanitarian air infrastructure was both overwhelmed and locked down, the UN established ‘humanitarian hubs,’ including at the Addis Ababa Airport, from which ‘solidarity flights’ transported medical supplies, humanitarian personnel and food rations across Africa.19 The WFP also began servicing tens of millions of households with direct cash transfers.20

In June, WFP launched the COVID-19 Global Response Plan, incorporating multiple strategies like logistical support to make up for the contraction of commercial transportation, household cash transfers, direct nutritional supplement, and expanding real-time mobile Vulnerability Analysis and Mapping (mVAM) to 39 countries, with calls to raise US$4.9 billion21 to support operations for the following six months.22 By November 2020, only half of this funding had been procured.23

The humanitarian projects in general faced funding shortfalls from the beginning—the Addis Ababa Humanitarian Air Hub only came online with donations from Alibaba CEO Jack Ma24—and this trend continued throughout the year, with grave impact. Many WFP country offices cut rations and reduced the number of beneficiaries. In the Democratic Republic of Congo (DRC), which has the largest population of people facing acute food insecurity in the world at 21.8 million,25 only 75% of required food rations were disbursed.26 In Syria, rations were lowered twice in the same year.27 By its own admission, WFP’s funding model of “total dependence on voluntary contributions” is “risky” and “particularly vulnerable to donor perception of priorities within its mandate.”28

In a year where the world’s billionaires expanded their private wealth by $10.2 trillion29 and governments faced budgetary crises, such dependence on the fickleness of philanthropic crumbs was shown to be a miserable affair. By October, WFP had transferred $1.7 billion in small cash payments to 97 million households—still only 35% of those in need—with a quarter of this coming from just 24 private donors.30 This was during the height of the L3 emergency, with WFP subsequently deactivating the L3-scale mobilization in November 2020.31

Funding shortfalls will continue to be a persistent problem as the sense of urgency amongst donors wanes despite the situation on the ground worsening. The WFP already at the beginning of 2021 anticipated donations decreasing by $400 million compared to 2020—roughly the same amount brought in from wealthy private donors for the already-inadequate cash assistance program.32 In the November report, WFP called for a further $7.7 billion to carry them through April 2021.33

Throughout WFP operations and beyond the COVID-19 Global Response Plan, funding against budgets for total humanitarian response plans stood at just 36.4% at the start of 2021.34 The 2021-2023 WFP Management Plan released in November 2020, identified a $4.9 billion funding gap relative to their projected expansions, as the economies of the prime donor countries contract, enforcing a “new normal in terms of resource mobilization.”35 This new normal has been precipitating for a while, however. The Development Assistance Committee nations of the Organization for Economic Cooperation and Development had committed to a goal of earmarking 0.7% of global national income for Official Development Assistance (ODA), which is a generic term for all governmental monetary aid including the bulk of WFP and other humanitarian organization funding. The goal was decidedly not met, falling an estimated $2 trillion short of the target since 2008,36 and the gap between requirements and funding for inter-agency humanitarian aid in 2021 is the “highest ever”, at $20.5 billion.37 A recent statement issued in November, 2021, claimed that WFP received just 45% of the $15.7 billion of funding they required for the year.

This endemic incapacity is all the more dire when taking into account prospects for the immediate future. Based on early warning signs yielded by the mVAM data, the Food and Agriculture Organization (FAO) and WFP released a joint report in October 2020, identifying 20 ‘hotspots’ where the populations are at high risk of acute deterioration in their already-stressed food security. Each of these countries was already included in the 55 countries analyzed in the GRFC, but now face significant exacerbations. Each has more than one ‘driver’ of insecurity converging in one place.

In the Democratic Republic of Congo, for example, conflict has displaced 6.6 million people in the countryside and destabilized many more, but food security is also collapsing in more peaceful urban areas, where many households that depend on an ‘informal economy’ have lost income due to COVID-19-related restrictions on market activity.38 In Cameroon, Boko Haram’s presence in the north of the country led to nearly a million internally displaced persons (IDP) since 2017,39 which has caused the acutely food-insecure population to double over the course of 2020 to 2.1 million.40 It is anticipated to more than double again over 2021 to 4.9 million.41 In Yemen, which “remains the world’s largest and most complex humanitarian crisis to date,” years of war have caused severe food price inflation of 140% compared to pre-war levels, prompting estimates that the acutely food insecure population would exceed 17 million by 2021 already before the pandemic.42

In addition, swarms of desert locusts—the world’s most destructive migratory pest—had infested 23 countries, with the epicenter in the Horn of Africa, but also affecting Yemen, Iran and the Indo-Pakistan border region.43 The default state of locust grasshoppers is to disperse as individuals; however, when vegetation is concentrated and patchy then the overcrowded populations undergo an auto-catalyzing phase transition called ‘gregarization’ in which they begin to swarm.44 Desert locust swarms can increase their population size 20-fold every eight weeks, with single swarms containing up to 80 million individuals, scouring up to 90 miles and eating the equivalent that a town of 35,000 consumes every day.45 Successful locust management requires proactive disruption of gregarization in its early stage; once the swarms begin to travel it is much more difficult to contain.

Prior to 2020, international cooperation spearheaded by the FAO, had all but curbed the plague: locust plagues occurred in 41 of the years between 1910 and 1963 (77%), but after implementation of management strategies, they only occurred in 8 of the 56 years since (14%).46 However, a unique convergence of factors has caused this outbreak to burst through the typical barriers and grow into one of the worst plagues in 70 years.

After tropical storm Mekunu hit Oman, the abnormally powerful storm continued across the Arabian peninsula instead of dissipating upon landfall as usual. Mekunu deposited torrents over the largely uninhabited ‘Empty Quarter’ (Rub’ al-Khali) in Saudi Arabia, creating desert lakes and moist, sandy soil perfect for locust eggs to hatch. Usually ‘wet seasons’ are short-lived in the superarid Rub’ al-Khali, which had not seen rainfall in the 20 years prior. The locust would have died off, but 2019 was a record breaking year in the north Indian Ocean, with the highest number of storm days on record, including the most Category 3+ storms, and twice as much accumulated cyclone energy as the second worst season.47 Mekunu was followed by tropical cyclone Lubun at the end of 2018 and then a series of storms throughout the 2019 season, which preserved and extended the optimal breeding grounds. Three generations developed and went undetected, increasing the population 8,000-fold before spreading.

The swarms first moved into Yemen, where the war scuttled any state capacity for environmental management. They were able to proliferate before tropical storm Pawan blew the swarms across the Gulf of Aden into East Africa.48 This pattern of inactivity in the face of proliferation repeated, as the East African Desert Locust Control Organization (DLCO), after years of underfunding due to austerity within the member countries, could not coordinate a response rapidly enough. In Somalia, as in Yemen, the ongoing conflict meant that some breeding grounds were not even accessible. With only four planes, a shortage of protective gear and the inability to import pesticides quickly enough due to COVID-19 lockdown restrictions, the DLCO could only watch the locust population cascade in the first months.49 This lost time was crucial. One swarm in Kenya grew to encompass 2,400 km2, or three times the area of New York City.50 Hundreds of thousands of hectares of agropastoral land were ruined over the course of 2020.

An international effort lead by the FAO did manage to control the spread westward, preventing the likely migration to West Africa in July, and treated 1.25 million ha. of infested land. But, in November 2020 tropical cyclone Gati, the first ever recorded hurricane-force cyclone powerful enough to make landfall in Somalia, deposited a year’s worth of rain over eastern Ethiopia and Somalia in a span of two days and created new breeding grounds to sustain the plague far into 2021.51

The centrality of anomalous storms to the severity of this disaster should not be overlooked. The consecutively record-breaking monsoon seasons can be explained by an extreme positive phase of the Indian Ocean Dipole (IOD), particularly in the last six months of 2019 when it was in its most positive state since 1870.52 The IOD is a mode of coupled atmospheric-oceanic variability, akin to the more famous El Niño-Southern Oscillation (ENSO), in which a sea surface temperature gradient between the western Indian Ocean and the rest of the basin drives weather systems and wind directions across the rim, determining rainfall in a large number of areas.53 The IOD is referred to as ‘positive’ when the western Indian Ocean mean surface temperature, which is typically cool, becomes warmer than the waters off the Java-Sumatra coast to the east. This pulls winds and moisture westward to dump it in the tropical African and Arabian coasts, in turn producing anomalously dry conditions in the eastern Indian Ocean rim. The kind of extreme positive IOD seen in 2019 is a rare event, occurring just ten times in the past 500 years, but one that is increasing in frequency, as four of those ten occurred in the last 60 years.54 The IOD not only caused aberrant flooding in East Africa and Saudi Arabia, but the dry end of the dipole played a role in the devastating bushfires in Australia in 2019-2020.

Since the western tropical Indian Ocean is the fastest warming tropical ocean region in the world,55 the mean state of the Indian Ocean is fundamentally changing and becoming more susceptible to extreme dipole reversals, and it is expected that the frequency of positive phases in the IOD will triple in the 21st century.56 This has already led, among other things, to declining mean rainfall (between 10-20%) on the Indian Subcontinent in regions still dependent on rain-fed agriculture at the same time as there has been a three-fold increase in the frequency of extreme rainfall events, simultaneously desiccating and flooding the countryside.57 Extreme cyclonic storms have increased in the Arabian Sea,58 with the three strongest cyclones to ever hit the Arabian peninsula occurring in the last 15 years and Somalia and Mozambique both receiving their strongest storms ever in the past two years.59 By the end of 2019, the lives and livelihoods of 2.8 million people in east Africa were affected by heavy rains, flash floods and soil waterlogging due to the IOD.60 Rain-soaked desert grounds ripe for locust gregarization events are likely to become a more regular feature of the east African and Arabian human landscapes.61

Now a much different climate event is developing. Though the extreme positive phase of Indian Ocean Dipole subsided by early 2020, in October the World Meteorological Organization declared the development of a La Niña episode, a cold phase of the El Niño-Southern Oscillation (ENSO) system, which is still ongoing as of December 2021.62

Besides the seasons themselves, the ENSO is the most important source of climate variability.63 Recurring weather structures emerge as solar energy absorbed along the equator dissipates toward the poles in a complex pattern mediated by zonal heat reservoirs. The waters between Indonesia and Australia, called the ‘Warm Pool,’ and its coupled atmospheric system, the Indo-Australian Convergence Zone, are the largest of such heat engines on Earth, sustaining a process of deep convection that functions as a massive ‘cloud factory’ conveying correlated climatic imprints to disparate corners of the world through meteorological ‘telecommunication.’64

While the exact impact of climate change on the ENSO is still an area of open investigation, it is possible ENSO variance may increase by 15% by the end of the twenty-first century, with extreme phases possibly doubling in frequency.65 This increased variance will make individual events much harder to predict or model in real time, which will inhibit readiness efforts. By trapping any excess heat retained by greenhouse gasses, in warm phases, and unleashing it in catastrophic displacements of wind and water, or alternatively sapping the same in cold phases, “an enhanced ENSO cycle […] may be the principle modality through which global warming turns into weather”—and therefore chronic food insecurity.66

After the devastating rainfalls and poor harvests of 2019, regions from the Central Asian steppes to the Levant and east Africa are experiencing severe dry spells, approaching drought conditions in some places. The expected La Niña duration will coincide with the peak growing seasons of the Philippines, Indonesia, east and southern Africa, Central America and the Caribbean.67 In Pakistan, reduced rainfall and snowpack will likely decrease wheat output.68 Similar conditions in Afghanistan may make crops more susceptible to deadly frosts.69 Somalia, Ethiopia and Kenya have all had ‘erratic’ rainy seasons, overly dry in some areas and wet to the point of flooding in others.70 Indonesia, on the other side of telecommunication, faces above-average rainfall and possible flooding and landslides.71 La Niña enters its second winter, trailing one of the strongest monsoon seasons on record causing agricultural damage in Vietnam and the Philippines.72 Turkey had already been experiencing a 50% year-over-year decrease in rainfall in 2020 and the onset of La Niña is threatening to push that to the brink of drought. In January 2021, Istanbul had just a month and a half’s supply of water, prompting the government to organize rain prayer ceremonies throughout the country. These rains came on a prayer, thus avoiding the most acute and immediate consequences, but, as of November 2021, Istanbul still faced drought, with every one of its reservoirs below capacity.73

This La Niña phase is actually considered relatively weak, but the correlation between the strength of ENSO events and agricultural stress is not clear cut: strong cycles tend to have large effects, but weak cycles can coincide with widespread famine as well, as the impact of natural phenomena only exists in the context of the whole system of vulnerabilities and interdependencies.74 It is therefore hard to predict the extent to which a season of disrupted planting, which would lead to the second underperforming harvest in a row in some places, will extend the food crisis. We have, however, reaped one benefit in the form of a force majeure: after continued locust swarms for the first half of the year, La Niña conditions dried out the East African and Arabian breeding grounds, “contained by poor rainfall.”75 The apocalyptic locust plague has subsequently subsided, although several swarms are still substantial in Ethiopia.76 As the FAO notes, this was due to sheer luck as 2021 proved to be a rather calm year after the sequentially record-breaking 2019 and 2020 storm seasons. Moreover, focusing solely on the projected impacts of ‘natural’ disasters, and locating the crisis within the aberrant convergence of freak accidents, threatens to obscure the social origins of the immiseration.

As already noted, the devastating pest and rainfall patterns are the result of exacerbating climate change, itself a complex interplay between anthropogenic destabilization and critical thresholds of runaway feedback. These ‘natural’ occurrences, whether swarm or storm, make landfall onto complex human terrain already criss-crossed with sociopolitical conflict. But then, so too are the ‘social’ phenomena inseparable from the environment in which they are embedded, the terrain shaped by the erosion of social metabolism, the accumulated tensions of tectonic class contradictions, and the great earthmovers of combined and uneven development. The intention of this article is not to merely present an empirical picture of the drivers of hunger, which will appear as an incomprehensible litany of disasters related only externally and contingently, but rather to take a dialectical approach to trace out the inner relations which constitute the present crisis. We now will turn to an exploration of chronic hunger and a sketch of the historical period following the eclipse of the ‘second food regime’ in the 1972–1974 food crisis.

2) Food Securities

Despite early worries, 2020 closed with food production at an all-time high. At 2.7 billion tons, world cereal output rose 1.3% over 2019.77 In east Asia, 2020 was the best year on record in terms of paddy output.78 In South America, farmers sowed the most land area ever, breaking output records for the second year in a row.79 In Low-Income Food-Deficit Countries (LIFDC), aggregate production stands at 496 million tons, about 7% above the five year average.80 Recalling our two questions in the previous section, what must be explained is the contradiction between high general food productivity and the prevalence of hunger.

This super-abundance fits with the trend of the past few years. Numbers like this reinforce the conclusion that the acute spike in world hunger in 2020 is highly circumstantial and contingent. But this would misapprehend the phenomenon: severe hunger cannot double from 135 million to 271 million in a year if vulnerability to food insecurity was not a widespread and chronic condition. Another breakdown of the estimates will shed some light on this. The severely food-insecure population reported in the original GRFC document to be 135 million constitutes everyone in Phase 3 (“Serious crisis”) and above, with about 27 million in Phase 4 (“Critical”) and 84,500 in Phase 5 (“Famine”).81 Beyond the 135 million classified at Phase 3 or above, an additional 182.6 million people were classified in Phase 2 or Stressed conditions.82 This latter category consists of people facing “uncertainties about their ability to obtain food and [therefore] a lack of consistent access to food, which diminishes dietary quality, disrupts normal eating patterns, and can have negative consequences for nutrition, health and well-being.”83 There is a thin barrier between this status and more acute manifestations of hunger, which is easily swept away at the sign of trouble, pushing the chronically hungry into the population of the acutely starving.

The way food insecurity is measured depends on how it is defined. Food security has four components—availability, utilization, access, and stability—each of which have their own dynamics and points of vulnerability. A previous report, The State of Food Security and Nutrition in the World, released in 2019, takes into account two different metrics to understand the scale of hunger.84 The first metric, prevalence of undernourishment (PoU), is derived from aggregated country-level data on food available for human consumption and from surveys.85 PoU indexes the availability and utilization of food sources, that is, direct hunger. The second, the prevalence of moderate or severe food insecurity (FImod+sev), uses surveys based on the Food Insecurity Experience Scale (FIES), in order to get a sense of what people have to go through in order to acquire food; the focus here is on access, or the consistency of the wider distribution and consumption network.86 The advantage of the latter measure is its applicability in developed countries, allowing for a truly global estimate. According to the global aggregation of PoU, as of 2019, 821.6 million people, or 11% of the world population, go hungry for at least part of the year.87 Taking into account (FImod+sev), in 140 countries, it was found that an additional 1.3 billion people did not have regular access to nutritious and sufficient food. This means that, as of 2018, 26.4% of the world’s population, or about 2.1 billion people, are either undernourished to the point of real risk of long-term health impacts or presently hungry and in imminent danger of starvation.88 These rates have risen every year since 2015.89

This tells a much different story than one in which hunger is circumstantial. This framing of ‘access’ is key to understanding the structuration of vulnerability. Food may be technically available in sufficient quantities, but inaccessible due to an inability to afford staple foods at their predominant prices. As Clapp and Moseley write, development policy since the food crisis of 1972–1974 has been oriented toward “improved food access through high levels of production that kept prices low on one hand and boosted farm incomes via specialization and commercial trade on the other.”90 The dominant pull over the last 50 years has been to draw the world’s agricultural systems—whatever their status of development—into a single world market.

Imperialist activity in the immediate postwar period had to quickly substitute the stability lost when the previous social order was destroyed by war. Of the capitalist bloc, only the US remained with substantial command over productive forces. As such, surplus American capital was necessary for the reconstruction of Europe and east Asia, confronting in the process a surge of decolonization struggles unleashed by the interregnum and a strike wave that spread throughout the industrialized world.91 As industrial development was insufficient to dispel the anticolonial and worker struggles, this precipitated a centralization in US agriculture and a series of agrarian programs and technological developments that would come to be known as the Green Revolution (GR), focused especially on grain productivity.

The GR is defined by developing farms toward a high organic composition of capital,92 with a premium on yield productivity achieved through high yield seed varieties, industrially-produced chemical fertilizer and pesticides, and heavy machinery.93 This cluster of policies was not only promoted by agribusiness interests, USAID, and philanthropic entities such as the Rockefeller Foundation, but was enthusiastically adopted by the governments of postcolonial countries eager to pursue strategies of agrarian reform and industrial transition, as following the path of development in western Europe and according to theories of Fordist ‘modernization.’

As food prices rose sharply between 1972 and 1974, with maize, wheat and soy prices tripling, concerns rose over the specter of food shortages, as the spike in prices was interpreted as primarily a problem of underproduction. The 1974 World Food Conference pinpointed ‘self-sufficiency’ through the adoption of GR technology as the prime goal.94 The result was that the remainder of the 1970s were marked by a ‘big push’ in production, both within the US (Secretary of Agriculture Earl Butz implored US farmers to plant crops “from fencerow to fencerow”),95 and abroad, through such self-sufficiency programs as state price subsidies and import tariffs. The result was developing countries approaching self-sufficiency and then net overproduction as prices began to substantially fall.

The Volcker shock, in which the US Federal Reserve raised interest rates in an attempt to curb inflation, made the steadily accumulating state debt, mostly for development infrastructure, practically impossible to pay off. The International Monetary Fund (IMF) and World Bank instituted debt restructuring, stipulating ‘adjustments’ to the state expenditures and regulations of recipient countries. This restructuring effectively abolished any notion of self-sufficiency for the recipient countries. Subsidy programs were ended, tariffs dropped in favor of free trade deals, and small subsistence farmers, encouraged to take on debt in order to purchase expensive capital inputs, were now exposed to the international market.96 The farming sector in major grain-growing countries, having gone through their own farming crises in which farming land was consolidated and concentrated under larger agribusiness firms who then contracted with the remaining smaller farms, were overcapitalized, overcapacitated and entirely reliant on the export of surpluses. This oversupply spurred innovations in the sciences of food processing, ushering in the abundant panoply of calorically-dense grain derivatives that fill many supermarkets across the world, the most important ingredient of which is high-fructose corn syrup, as well as major markets in bio-ethanol and animal feed.97 During this time, the emphasis transferred from developing technically sufficient food systems to identifying market niches in specialized commodities, a process promoted and exacerbated by coerced trade ‘negotiations,’ bringing into being the World Trade Organization (WTO) in 1995.

The trade agreements reached through this system, which formalized cross-national markets purportedly open to firms from any country with no preference, had the effect of skewing the markets in the direction of the agricultural industries in the developed countries, which by 1986 benefited from $300 billion in subsidies a year.98 Food prices remained low throughout the 1980s and 1990s, devastating what remained of the smallholding peasant class, who began to supplement their production with part-time, and then increasingly full-time, wage work.99 Low food prices incentivized food producers to merge or sell to agribusiness firms, vertically integrating diversified operations spanning farm equipment, proprietary seed varieties, chemical inputs, food processing, and distribution.100 Agricultural trade increased at an annual rate of 4% between 1990 and 2002, twice the rate of agricultural production growth.101

Today, around 20% of dietary calories are supplied by imported food and 80% of the world’s population is fed at least in part by imports.102 Trade does not just refer to finished goods that are destined for consumption, but also inputs and intermediary products, to the point where even ‘domestic’ food chains depend on international imports at some point. The term ‘net importer/exporter’ is somewhat outdated, as many countries tend to do massive amounts of both, even if the net is in one direction. For example, in sub-Saharan Africa 75–90% of food consumption derives from domestic supply chains, but as a whole the region is a net importer of food.103 This interdependence is a stark departure from the heyday of modernization: Côte d’Ivoire, for example, was nearly completely self-sufficient in rice production by 1976, but by 1990 half of domestic demand was met through imports.104 The doctrine of ‘food security’ itself emerged in this period, as the premium of development is not placed on any kind of development of bioregional resources for domestic consumption needs, but rather the strictures of global competition and the need to carve out a place within the international market system. ‘Food security’ comes from purchasing power, not agricultural productivity. Adequately providing for the entirety of the population depends, then, not on robust agroecology and public provisioning, but on ensuring that food stores are filled through imports. Hunger is staved off in the current food regime not through development of production, though advances in agrarian science could theoretically accomplish this, but through the maintenance of incomes, which is fundamentally uncertain and subject to active suppression from capital abroad.

Trade interdependence is a form of structural vulnerability, which manifests in two distinct ways as a result of the COVID-19 pandemic. First, because most world subsistence is mediated by the market, following the real subsumption of social reproduction into commodity relations, the contraction in income has effectively cut off many people from their accustomed food intake levels—a problem of access more than availability. Outside of the perpetually underfunded humanitarian relief apparatus, which has a highly ideological notion of “emergency” that triages the disbursement of funds to only the most acutely undernourished, there is no stable institutional supplement to household food supply. Second, the concentration of capital in agricultural production and, especially, distribution, have created the conditions for supply chain shocks to roll over into financial markets and back again. Trillions of dollars worth of credit instruments depend on food commodities trading at certain prices, and these prices in turn depend on a given background rate and volume of trade. The goods have to keep moving for the entire edifice to remain in place; any significant slowdowns or stoppages will lead to obstacles in other markets.

Extensive agricultural value chains could only operate through the intensive penetration of international finance. This capital, like all industrial capital,105 is substantially and increasingly centralized. Financial entities are increasingly involved in food retailing, processing, commodity trading, price determination, agricultural input production and provision, and the ownership of land.106 They constitute what Jan Douwe van der Ploeg calls “food empires,” large networks controlling the production, processing, distribution and consumption of food, to appropriate the value produced in agriculture.107 One study found that, by 2009, the four largest firms in each of the five categories of agricultural inputs—agri-chemicals, seeds, animal pharmaceuticals, animal genetics and farm machinery—accounted for 50% of global market sales.108 Seeds and agri-chemicals in particular are interlocked, with the largest six firms in each sector, collectively controlling 60% of the global seed trade and 75% of the pesticide market.109 The watershed moment of monopolization occurred in 1996 when several ‘life sciences’ conglomerates introduced genetically-modified plant varieties that were resistant to proprietary pesticides sold by the same companies, such as the RoundUp Ready line of crops sold by Monsanto.110 Since then mergers and consolidations have accelerated, faster than in any other sector, with thousands of small seed, biotech and pesticide startups merging into just six firms by 2009.111 Livestock chains are highly vertically integrated, with genetics-breeding, pasturing, slaughter, and animal pharmaceutical companies increasingly merging and collaborating in order to run concentrated feeding operations.112 Fertilizer companies, whose production chains depend on mineral extraction, are comparatively much more bound to scarce land. Nevertheless, GR farming methods, which are the foundation of most agronomic research and development today and lay at the root of most farms producing for sale, crucially incorporate artificial fertilizer. This dependence has led to the development of state-sanctioned export cartels based in a handful of developed countries—primarily in the US, Canada, Russia, China and India—which dominate world markets; the top ten firms account for 56% of global sales.113

Though this trend matches the general centralizing tendency of the law of value,114 agribusiness especially has experienced substantial consolidation, for several reasons. First, agriculture has fulfilled numerous crucial roles in different periods of imperialism. The plantation system of the colonial periphery, with the use of unfree labor, successfully extracted a steady flow of inputs into the metropolitan industrial apparatus (crucially cheapening European labor-power), enabling the “culmination of colonialism” into a coherent ‘drainage’ system tilted towards the imperial cores.115 Later, in the putative second food regime, Western food aid and grain commodity exports formed a plank in the Cold War geostrategy of containment, used to extend the state system to the decolonizing periphery and preemptively disrupt nascent communist and rural populist movements.116 Subsequently, with the Green Revolution, agricultural development and food security became the impetus for the export of overaccumulated capital in the form of readily consumed circulating capital, with the value-added returning to be realized in the Global North with the construction of commodity chains and the extension of the downstream food processing sector.117 Second, farming resists subsumption into the value-form, as it involves the direct metabolic transformation of nature, tied to valueless land118 and turning over with the tempo of the seasons, making it challenging to reconcile agricultural commodities with socially necessary labor-times. This incentivizes investment into up- and downstream processes, where value-measure is much more coherent, as a means of subsuming agriculture by way of commodifying its components. Third, the ‘auto-producing’ quality of crops, agriculture being a reification of ecology, paves the way for the post-biotech explosion of rent-seeking capital and a race to lock down intellectual property patents on the genetic and biosynthetic process information involved.119 Finally, food trade is important for the global system and for realizing the value of overproduced goods. As will be explored below, such extensive trade networks could never be organized without a comprehensive credit system meaning that, despite its appearance as the preeminent ‘real economy,’ it is one of the more financialized sectors, facilitating a mountain of contracts and paper titles dramatically altering land use and subsistence across the planet.120

The food conglomerates of the future will all but completely vertically integrate the entire supply chain. A common technical determinant in the concentration and profitability of the agricultural input sectors has been the central role of major advances in data analytics. Seed and pesticide companies have developed massive control databases on soil, weather and crop yields, which equipment companies have begun to license and incorporate into data-integrated farm equipment. Tractors, combines, sprayers, reapers and other equipment are equipped with digital tools such as remote sensing, wireless access to data servers, and aerial imaging, informing farmers where and when to irrigate, fertilize and plant.121 Next generation tractors are controlled by GPS rather than drivers, and drones are being increasingly marketed in pesticide spraying, monitoring, and even pollination. One of the most vertically integrated agricultural input firms in the world, Mahindra and Mahindra in India, makes $17 billion a year in sales across 20 sub-sector industries, including equipment, pesticides, seeds, fertilizers, irrigation tools and soil testing.

The higher tech corporate products are not universally or even widely available. But they represent a number of features of agricultural production. First, most of the money made in agriculture is not made by farmers. As Levins and Lewontin wrote in 1985 at a much earlier stage of this process, “the effect of technology has been to reduce the value added on the farm and increase the value of purchased inputs. That is, the chief consequence of technological innovation to increase on-farm productivity has been to make on-farm productivity less and less important in determining agricultural value.”122 Second, as a result of this political economy, smaller farms are having to take on more expenses, and therefore more debt, to afford the chemical inputs, proprietary hybridized and GMO seeds, and ‘digital revolution’ equipment, which is concentrating farming capital. Nowhere is the impact of this more stark than in rural India, where 42,480 farmers and agricultural day-laborers committed suicide in 2019 as a result of the debt crisis.123 India’s further integration and subordination to global capital during the Modi government was recently stopped through nationwide resistance.124 Third, in the context of international markets, the proliferation of these technologies will increasingly define production conditions in general, and will therefore set the pace of output and dominate the price structure. And finally, as farming becomes more capital intensive, the role of trade will become more central, even to food consumed domestically.

While large agricultural input firms have dominated production, distribution has been dominated by competition between large commodity trading clearinghouses and food retailers. The big four commodity traders—Archer Daniels Midland (ADM), Bunge, Cargill and Louis Dreyfus—are thought to account for 90% of the global grain trade,125 having dominated since the 19th century, but are recently joined by Singaporean and Hong Kong traders such as Noble Agri, Olam and Wilmar, and Chinese state-owned firm COFCO, as well as mineral and energy traders.126 The combined income from the top six agricultural commodity traders was $364 billion in 2016, more than the combined global markets for seeds, equipment and pesticides.127François Chesnais argues that, when viewed in the broader context of the intermeshing of banks, industrial corporations and retailers, such profits, which seemingly derive from circulation itself, are dependent on maintaining monopoly and monopsony shares of the capital circuit.128 In other words, high profitability relies on control over the globalized agricultural value chains, the values produced on farms across the world concentrating in the hands of these few firms. Because the circulation of food and upstream agricultural commodities is a central site of profitability, driving the growth in trade volume, the acquisition and consumption of food depends on the maintenance of certain market structures.

These major food empires could not exist if it were not for a robust credit and risk securitization system. Besides the role of financial equity in corporate mergers and acquisitions, the chains themselves operate only by virtue of the cycling of credit. Each company is managing the flows of many types of commodities entangled in large interdependent price networks, such that the whole flow is sensitive to price changes. Flexibility is key, and therefore financial securitization and insurance instruments like futures, commodity index funds, and export credit assurances are central to the circulation of food.129 Because food is perishable and traded at a large scale, short-term credit infusions are necessary. Food ingredient deliveries are made on credit, to be paid back in 90 days typically. This risk is offset with the purchase of a trade credit insurance contract with a third-party company. The seller, waiting for their payment but incurring costs of their own, will purchase more productive capital and pay wages with a bank loan, using this credit insurance as collateral. The credit rating of the seller is then the crucial modulating factor in this particular commodity flow: with a good rating, this gap in value realization can be bridged with the successful flow of credit, paid out either from the buyer coming through or the insurance. If the seller is rated poorly, then high rates of interest will be imposed. Global agricultural commodity chains are stitched together through such relations, making them highly sensitive to risk and insolvency.130

Food empires, since they are based on positionality within trade flow networks, primarily accumulate through lateral growth in markets. Most food empires, whether retailers, commodity traders or some other variety, are therefore constructed using monumental debt loads which enable them to acquire and consolidate along the value chain without relying solely on in-house profits. The debt to capital ratio of Cargill, for example, is fifteen to one.131 In 2008, market volatility drove the trade credit insurance companies to withdraw, effectively halting the flow of food commodities, driving already spiking prices up even higher.132 In 2020, the closure of many restaurants and catering companies led to a net contraction in food demand and subsequently many rounds of canceled contracts. These canceled contracts have backed-up supply chains and, since so many agricultural regions are intensively specialized they have wreaked havoc on national incomes.

One very telling example should suffice. In Kenya, horticulture has become 21.4% of the value of exports (as of 2018), with much of the agricultural land devoted to fruit, vegetables, flowers and herbs.133 Over 80% of these exports are shipped to the EU. The high perishability of these goods means that they are shipped on the cargo holds of passenger planes. After COVID-19 struck, there was a wave of contract cancellations, as well as the grounding of most flights. This cessation in the flow of goods left them abandoned in Kenya where, despite the aforementioned food insecurity and locust plague, the crops were left to rot, as most local people could not afford the prices commanded by these crown jewel export commodities of this development success story.”134

This pattern has repeated innumerable times in the span of the pandemic, with single specialized lines dependent on export markets suddenly finding themselves burdened with a glut of now-overproduced commodities, and unable to sell them in local markets. Though global prices of staple crops have remained relatively stable thus far, there have been many instances of local price inflation, driven by these supply chain backups. The impact of these lost sales has percolated up through the value chains, affecting much of the activity within the food empire networks. The situation has not yet reached the crisis proportions of 2008, with a systematic withdrawal of credit, but insolvencies are steadily accumulating throughout the food trade sector and, as canceled and missed contracts abound, the insurance ratings upon which the trade credits are based are creeping downwards.135 Coface, one of the big three providers of trade credit insurance, released an industry ‘barometer’ in August 2020, forecasting that corporate insolvencies would increase by a third in 2021 affecting trade in every commodity sector.136

3) Peasant Mobilities in the Era of Labor Demobilization

World food prices, on the whole, declined for much of 2020, as have most commodity prices in the 2020 economic contraction, but there have been wrinkles in this trend that have produced local eddies of spiraling prices. Different countries have experienced widely divergent levels of food inflation. Switzerland, for example, experienced an increase of only 0.7% in local food price between February and July 2020; Guyana, on the other hand, underwent a 49.8% increase.137 The distribution of price increases is rather large and some patterns are discernible. Half of the countries with the highest price increases are dependent on food imports.138 These dependent countries are sensitive to changes in supply chains. Staple food stocks are highly concentrated, with China, India, and the US claiming 65% of global grain stores.139 These stocks in grain-exporting countries are kept in order to maintain the market price structure, while importers scramble to make up for shifts in trade flows. The World Bank, confident that the ‘initial conditions’ (oil prices, food stocks, and weather) were favorable in 2020, was sure to ascribe any shocks to ‘uncooperative trade policies,’ cautioning against reactive trade restrictions.140 The International Food Policy Research Institute closely noted in April that trade restrictions in 19 countries resulted in a 61% reduction in food Kcal in Afghanistan, drawing the conclusion that free trade must flow in order for surpluses to be transferred to deficit areas.141 The FAO warns that countries will lose their competitive advantage in the world market if they implement export restrictions and attempt to build domestic stocks.142

This situation can be summarized as follows. Local subsistence systems, whether based in peasant households and patriarchal forms of labor exploitation or based in entrepreneurial farms,143 have been reorganized as nodes in agricultural value chains in many places such that the world market is the dominant means of obtaining agricultural goods for most of the population. This has had the effect of positioning postcolonial developing nations and peripheral regions as dependent on trade in a double sense: production is organized for export, and increasingly capital-intensive farming operations must export overproduced crops in order to turn a profit; and food security itself, in terms of adequate per capita access to nutritionally dense and complex food in sufficient quantities, is dependent upon imports.

The world’s staple foods are dominated by grain- and meat-exporting countries in the global North, which has two effects. First, the most important food prices are regulated by the profitability of agribusiness food empires, which then set the income level parameters that dependent countries must maintain in order to preserve food security. Second, ‘developing’ countries turn to specialized fruit, nuts and specialty items in order to command a place in the market. Falling prices in these specialized agricultural commodities can hurt the farmers dependent on these export markets, while rising prices of staples can make the dietary basics unattainable. Furthermore, all crops of any kind largely depend on imports of industrial inputs, which are increasingly monopolized, as described above. With the kinds of unpredictability and disruptions brought about by the pandemic, supply chain bottlenecks and local labor shortages (as the movements of migrant laborers are restricted) can lead to intense and compounding price volatility in the most trade-dependent countries.

This dynamic manifests in a number of ways. Exports of staples like rice, wheat, and potatoes have declined 15%, hitting heavily import-dependent countries like Lesotho, Mexico, and Jamaica, where 95% of staple imports are sourced from the dominant staple producers.144 In March, the UN Conference on Trade and Development estimated that the loss in export revenues amongst developing countries as a whole in 2020 will be roughly $800 billion.145 The FAO reports that the pandemic is not causing precipitous declines in world food stocks, as occurred in 2008, but that the loss of income from disappearing wages, lost opportunities for small proprietors and reductions in immigrant remissions has undermined purchasing power for many in poor and dependent countries. This loss is compounded by capital flight. Net outflows of foreign direct investment in emerging economies amounted to $59 billion in the first month after WHO declared the pandemic, more than double the outflow experienced by the same countries in the aftermath of the 2008 financial crisis.146 This situation has placed pressure on the international reserves of many countries, in many instances depleting and sending exchange rates spiraling. Currency depreciation against the dollar was worse in some places than in 2008.147 This has caused a vicious circle of depressed demand, saddling the aforementioned small proprietors with unsaleable stocks, with prices dropping for many agricultural products. There has been a year-over-year decline of 37% across commodity prices in 2020.148 At the same time, end point prices in heavily import-dependent markets, especially in urban areas where most food is purchased and distributed for the most people, are sharply rising. This is because of breaks in the logistical networks which connect rural areas which supply most of the inputs with the urban points of consumption.149 The index for food prices has risen roughly 30% since the beginning of 2020.150 The price structure upon which many precarious and impoverished food producers and distributive actors rely collapses along with the cessation of global trade, causing artificial shortages and price surges to appear at acute points in the world’s megacities. Food rots in the fields and products are destroyed to prevent against gluts, local markets, and urban distribution networks which feed the majority of the world’s population face shortages: these are twin faces of a commodity market system cleaved in half by collapsing incomes, use-values lying fallow from the season-like vicissitudes of value, compounding irrationality like a force of second nature.

By far the largest factor in food insecurity, however, is the contraction of household incomes. The crux of the issue is purchasing power. Food and other commodities flow to centers of disposable income, skipping over any regions where demand is not ‘effective.’ As global ‘de-peasantization’ has proceeded with the concentration of agricultural capital, necessities for the average person are increasingly procured through the market, with little alternative for subsistence outside of small plot cultivation. In this sense, access diverges from availability, as food stores, whatever their level, are locked up behind the mediating nexus of rising prices. The process of cyclical concentration of capital is accompanied by a concurrent process of ‘accumulation of labor-power,’ even as the organic composition of capital expels more and more laborers from its activity.151 The multiplication of the proletariat is a process of dispossession and deprivation, in which dependence on the social wage fund is enforced regardless of the conditions of the labor market. In other words, the capacity to afford food is subject to the contingency of employment amidst waning global prospects.

Between 1980 and 2000, the global workforce doubled in size.152 Between 2000 and 2019, a further 1.3 billion workers were added to the global workforce.153 These increases mainly came from the absorption of workers following the full integration into global capital of the USSR and China (who were not previously counted), but significant segments also came from a wave of land grabs from agribusiness and extractive industries,154 and from debt traps, where subsistence peasants forced into the market take out loans and microfinance to counteract losses from intensified global competition, effectively abolishing the smallholding peasantry as a significant class and pushing them to the margins of the market in labor-power as new proletarians.

As Farshad Araghi argues, after WWII, the construction of developmental states in the Third World, whether clients of the US, affiliated with the USSR or ‘non-aligned’, entailed programs of agrarian reform and rationalization.155 Whether through state collectivization or market consolidation, this had the effect of depopulating the peasantry; significant urban growth took place in this period. However, especially in the regions forcibly integrated into the bloc of US-aligned and unambiguously capitalist states, policies were often implemented which sought to preserve family-scale subsistence farming, and to develop subsidy programs that would integrate them into a market distribution system to, in theory, ramp up a surplus. There were many local reasons, not the least of which was the demands placed upon the state by peasant populations themselves, but a prime driver of this was to cultivate, via clientelism and patriarchal family structures, a population inured against the draw of revolutionary movements. In short, agricultural labor was being restructured on the global scale, but this process regionally varied in contradictory directions, with many enticed or forced off of the land and still others incentivized and supported in remaining, such that the net direction tended towards depeasantization, but only relatively.156 Land owned and cultivated by small (<2 hectares) farmers increased as a proportion of agricultural landowners as the average plot size shrunk; peasant populations were retained or produced, while land ownership in general concentrated into fewer hands.157

After 1973, the process of depeasantization accelerated in nearly every country.158 The aforementioned food and farming crisis of the mid-1970s enabled a retooling of existing policies. The intricate system of tariffs, price controls, state purchasing agreements, quotas and subsidies which formed the agricultural development policies was eroded in favor of liberalization. Subsistence farmers were exposed to the world market prices, dominated by the significantly more capital-intensive and state-supported farming sectors of the big exporter countries. In the same period, wheat production in Africa, Asia and Latin America began to decline, all of which were once surplus producing regions.159 The reigning ‘wisdom’ foisted upon developing nations was agricultural specialization and comparative advantage. In a country like South Korea, industrial policy was already heavily export-oriented and the decades of occupation by the Japanese meant that agrarian reform could proceed without gravely disrupting the balance of class forces.160 By the 1980s, South Korea was largely depeasantized, with industry proportionately absorbing this population. But these conditions were afforded by historical opportunity, nowhere near ubiquitous in the period of decolonization. In countries like India, Mexico, and South Africa, which are each unique but align with the general dynamic, no such proportionality was achievable. Instead, depeasantization has been catastrophic, resulting in impoverishment, social dislocation and migratory movement, while agribusiness has benefited from the clearing of the land.

Contrary to past patterns experienced by early capitalist powers, mass proletarianization has not been met with proportional employment in industry.161 In the same period of mass de-peasantization, there has been a global trend towards deindustrialization of employment in all national income quintiles, with 1990 as a major turning point.162 The onset of deindustrialization is occurring at lower and lower per capita GDP and manufacturing share of GDP and employment, meaning that newly industrializing countries are reversing the process.163 This is particularly evident in sub-Saharan Africa, where many countries had not properly begun to industrialize before this period began.164 There is a persistent global decline in labor demand and in labor share of income, as the labor process is reorganized, wage growth is suppressed through (among other things) global labor arbitrage, and barriers to foreign direct investment are opened.

This tendency has led to the growth of the ill-defined ‘informal sector,’ comprising 61% of the total global workforce and composed of casualized, often unwaged and coerced piecework in construction, manufacturing and services, where roughly two billion workers eke out a living.165

The first year of the pandemic has seen the broadest collapse in per capita incomes since 1870.166 According to the International Labor Organization, 345 full-time equivalent jobs were lost in the first nine months of 2020, equalling 20.7% of total jobs in the world.167 The UN Office for the Coordination of Humanitarian Affairs predicts that somewhere between 88 and 115 million people will slide down into extreme poverty that would not have otherwise.168 Some 80% of the workers in this sector have had their incomes affected by COVID-19 restrictions.169 Globally 800 million people depend on remittances from loved ones who have migrated for work.170 The World Bank reports that remittances fell by 7% in 2020.171 Recovery has been hampered by the recurrent spikes in COVID-19 outbreaks. The most recent ILO report on the state of global working conditions notes that 2021 was 4.3% below pre-pandemic levels, equivalent to 125 million full-time jobs.172 As a consequence, the ILO warns against a “great divergence”173 or “dual recovery” between developed and developing nations, as the recovery fails to take flight in many poorer countries.174 Van der Ploeg describes the consequences of this dynamic of interdependency. ‘Labor-importing’ countries in the Global North lose harvests due to lockdowns, and the largely migrant agricultural workforce subsequently loses income. Besides the contraction of imports of these food items into the trading partners which may affect dependent developing countries, the loss of remittances flowing into the ‘labor-exporting’ countries prevents those dependent families from accessing food, resulting in a concomitant drop in domestic demand that in turn affects the incomes of local farmers.175

The coronavirus pandemic is occurring in a highly connected, globalized world. The nature of these connections are very peculiar, deriving from social relations of production oriented towards profit and capital accumulation before anything else. As such, a handful of companies constituting the vast majority of the capital invested into world food production and controlling, indirectly, a significant portion of its arable land, dynamically alter the flow of food goods, processing them into a plethora of ‘value-added’ foodstuffs and industrial input materials. This structure does not exist in order to purposely starve any segments of the population, but nonetheless builds vulnerability directly into the system, insofar as sustenance is incidental to profitability.

As liberalized trade and a rising organic composition of agricultural productive capital pushes smallholding peasants out of their market, off their land and into the world of waged work, many are unable to secure consistent paying work. The ‘informal sector’ enables the circulation of incomes almost entirely outside the wage system. Of the two billion workers in this ‘informal sector,’ 76% of them have been significantly affected by the coronavirus pandemic.176 The social safety net, which might define a ‘floor’ of subsistence and make the requisite goods available for all, exists only in the stressed humanitarian networks which by nature only respond once the disaster has struck, so to speak.

The hardest hit areas appear to be the result of sheer bad luck, but to place too much stock into this appearance would be to miss the real stakes of the food crisis. First, persistent underdevelopment is a consequence of the structure of the markets in food, a structure built over many decades through an ad hoc process defined most of all by imperial powers competing to exploit the resources and labor of the periphery. Second, the seemingly ecological causes of food shortages are internal to the effects of the capitalist economy, as, among other things, the labor shunted out of the agricultural sector has been replaced with incredibly fuel-intensive machinery and inputs. The agricultural sector accounts for a full 24% of global greenhouse gas emissions; the transportation system, which nearly all agricultural products enter into, produces another 14%.177 The massive capital outlay required to compete in agricultural markets necessitates producing according to the scales demanded by export. The resulting density of trade requires the rampant overuse of petroleum. Finally, strictly speaking, there is enough food to feed everyone. There always is. But, on the whole, food stores are used to maintain price levels, not as reserves for the hungry. Without control over global food prices, or at least dependability of prices, many of the connections that constitute the most profitable food empire networks would not be possible. In order to “keep markets working,” overproduced food must be stored rather than distributed. Capital at large, unable to profitably exploit the labor of the world’s hungry, is unmoved by their hunger.

- Friedman, Harriet. 1993. “The Political Economy of Food: a Global Crisis.” New Left Review. 1(197): 29 – 57. http://www.wphna.org/htdocs/downloadsmay2012/Harriet%20Friedman%20The%20Political%20Economy%20of%20Food%20pdf.pdf; p. 31.

- Friedman, Harriet and Philip McMichael. 1989. “Agriculture and the State System: The rise and decline of national agricultures, 1870 to the present.” Sociologia Ruralis. 29(2), p. 95.

- See Aglietta, Michel. 1979. A Theory of Capitalist Regulation: The US Experience. Verso Books.

- Ibid.

- Friedman 1993; p. 38.

- McMichael, Philip. 2009. A food regime genealogy. Journal of Peasant Studies. 36:1. 139-169.

- As McMichael (2009) points out, “the ‘food regime’ can be considered to be simply an analytical device to pose specific questions about the structuring processes in the global political-economy, and/or global food relations, at any particular moment. Here the ‘food regime’ is not so much an episodic structure, or set of rules, but becomes a method of analysis.”

- McMichael 2009.

- The tripartite scheme is an analytical tool Braudel developed while writing The Mediterranean and the Mediterranean World in the Age of Philip II. Referenced in McMichael, Philip. “Land grab and the global food economy.” Presentation at SAMKUL-konferansen, Trondheim, 2014.

- For a discussion of the metabolic rift, see Foster, John Bellamy. 1999. “Marx’s Theory of Metabolic Rift: Classical Foundations for Environmental Sociology.” American Journal of Sociology 105, no. 2: 366-405.

- The GNAFC is an international coalition that formed in 2016 at the World Humanitarian Summit as part of an emerging paradigm referred to as the “humanitarian-development-peace nexus.” It encompasses 16 intergovernmental organizations, including the UN World Food Programme (WFP) and the EU Food and Agriculture Organization (FAO).

- Global Network Against Food Crises. 2020a. “Global Report on Food Crises 2020.” Food Security Information Network. (April) https://docs.wfp.org/api/documents/WFP-0000114546/download/?_ga=2.110164812.839036316.1594523860-600778378.1591470572.; p. 2. The original number of 135 million was derived using a scaled classification system called Integrated Food Security Phase Classification (usually abbreviated IPC), originally developed by the FAO to analyze a food crisis in Somalia in 2004 and then adopted as a global standard by the UN and subsequently diffused throughout the humanitarian NGO network; see IPC “Overview”. There are five Phases: 1 — Generally food secure; 2 — Chronically food insecure (Stressed); 3 — Acute food insecurity (Emergency); 4 — Crisis; 5 — Catastrophe, which is also the point in which international monitors will use the word ‘famine’; See Table 1 on p. 14 of GRFC 2020a.

- Ibid; p. 21.

- Anthem, Paul. 2020. “Risk of hunger pandemic as coronavirus set to almost double acute hunger by end of 2020.” World Food Programme Stories, (April).

- World Food Programme. 2021. “WFP – saving lives, preventing famine.” World Food Programme Blog, November 15, 2021. https://www.wfp.org/stories/wfp-saving-lives-preventing-famine; p. 5.

- Anthem 2020.

- World Food Programme. 2020b. “WFP Global Update on COVID-19: November 2020 – Growing Needs, Response to Date and What’s to Come in 2021.” https://reliefweb.int/sites/reliefweb.int/files/resources/WFP-0000121038.pdf.

- Sova, Chase. 2020. “How WFP Classifies Crises and Why COVID-19 Is at the Top.” World Food Programme Blog, April 14, 2020. https://www.wfpusa.org/articles/understanding-l3-emergencies/.

- WFP 2020a.

- WFP 2020b; p. 11.

- Unless otherwise noted, monetary sums will be denominated in US dollars.

- WFP 2020b; pp. 4, 7, 20.

- Ibid; p. 20.

- WFP 2020a.

- International Panel on Climate Change. 2014. Climate Change 2014 Mitigation of Climate Change. Cambridge University Press.

- WFP 2020b; p. 4.

- Ibid.

- World Food Programme Funding Office. 2020. “Strategic Evaluation of Funding WFP’s Work.” Evaluation Report 1 (May). https://docs.wfp.org/api/documents/WFP-0000116029/download/, p. 85.

- UBS. 2020. “Riding the Storm: Market Turbulence Accelerates Diverging Fortunes.” https://www.ubs.com/content/dam/static/noindex/wealth-management/ubs-billionaires-report-2020-spread.pdf.

- WFP 2020b; p. 4. The exact number was $403 million.

- Ibid; p. 10.

- Ibid; p. 21.

- Ibid.

- Global Network Against Food Crises. 2020b. “FAO-WFP Early Warning Analysis of Acute Food Insecurity Hotspots – October 2020.” https://docs.wfp.org/api/documents/WFP-0000120561/download/, p. 22.

- World Food Programme Executive Board. 2020. “2021-2023 World Management Plan.” Resource, financial and budgetary matters, (November). https://docs.wfp.org/api/documents/WFP-0000119403/download/.

- UN Conference on Trade and Development. 2020. “The Covid-19 Shock to Developing Countries: Towards a “whatever it takes” programme for the two-thirds of the world’s population being left behind.” Trade and Development Report Update, (March). https://unctad.org/system/files/official-document/gds_tdr2019_covid2_en.pdf, p. 11.

- United Nations Office for the Coordination of Humanitarian Affairs. 2021. “Global Humanitarian Overview 2021.” (December). https://2021.gho.unocha.org/.

- WFP 2020b; p.16.

- UN High Commissioner for Refugees. 2019. “2019 Year-End Report, Operation Cameroon.” Global Focus: UNHCR Operations Worldwide. https://reporting.unhcr.org/sites/default/files/pdfsummaries/GR2019-Cameroon-eng.pdf.

- WFP 2020b; p. 15.

- Food and Agriculture Organization. 2020b. Cameroon | Revised humanitarian response (May–December 2020): Coronavirus disease 2019 (COVID-19). http://www.fao.org/3/cb0192en/CB0192EN.pdf

- WFP 2020b; p. 18.

- Kray, Holger, and Shobha Shetty. 2020. “The locust plague: Fighting a crisis within a crisis.” World Bank: Voices, April 14, 2020. https://blogs.worldbank.org/voices/locust-plague-fighting-crisis-within-crisis.

- Despland, E., Collett, M. and Simpson, S. J. 2000. Small-scale processes in desertlocust swarm formation: how vegetation patterns influence gregarization. – Oikos 88:652–662.

- World Bank. n.d. “The World Bank Group and the Locust Crisis.” World Bank. https://www.worldbank.org/en/topic/the-world-bank-group-and-the-desert-locust-outbreak.

- Maynard, Christine, Michel Lecoq, Marie-Pierre Chapuis, and Cyril Piou. 2020. “On the relative role of climate change and management in the current desert locust outbreak in East Africa.” Global Change Biology 26 (April): 3754.