I'm grateful for Gary Levi's Letter regarding my recent essay on the 21st Century Capitalist, which raises an important issue I did not elaborate much on: the alternative hypothesis for a lack of investment in neoliberalism being a certain level of unprofitability in the economy. The logic goes something like this: capitalists have an immense hoard of cash that they would quickly invest if there were any such opportunity to do so, but due to the level of development and lack of dynamism in the economy, no such opportunities exist. Hence, the secular stagnation of neoliberalism is ultimately reducible to technical conditions for profit-making, rather than capitalist decisions to consume rather than invest, as I had claimed.

However, due to a number of facts, it is not possible that the issue here is that capitalists cannot find investments equal or greater to the average rate of profit.

The first such fact is that capitalists, of course, do not know the actual profit rate of a given project in advance. Rather, capitalists, when underwriting a given project, will necessarily have to assume an average or higher rate of profit for the given industry they are investing in. Certainly, many capitalists will walk away from an investment opportunity if they suspect that this rate of return will not bear out, but there is indeed no shortage of investment opportunities floating in the aether that loudly proclaim an average or higher rate of return.

Two, we should expect that given greater hoards of financial capital, there should be ever more supply of entrepreneurial capitalists proposing such projects. And if we compare between countries that have large and highly liquid financial markets with those that don’t, we do indeed see a corresponding difference in the quantity and quality of capitalist suitors seeking cash. Marx himself assumed that an over-accumulation of financial capital would necessarily lead to an over-accumulation of the means of production and therefore an over-accumulation of commodities. Why exactly has there been a break in this logic? The thesis, which attributes this to a lack of profitable opportunities, doesn’t particularly explain this; rather, it is meant as a self-evident brute fact: if capitalists are not investing in fixed capital, it is because there is not reason to do so.

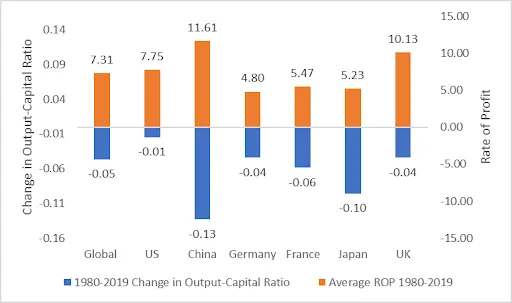

But this is an issue that can also be examined empirically. In my piece, I talked about how the position of the US and UK is somewhat unique in the global economy. Their roles in the global financial system afford them the ability to maintain simultaneous large trade and government deficits, as well as have lower investment compared to their peers. Here, I’ve decided to illustrate this further in the graph below.[1]

The change in the output to capital ratio, or the GDP to fixed capital stock ratio, can be thought of as a proxy for investment here; when it is falling, it means the capital stock has grown relative to GDP (since we know all these countries saw both real and nominal growth between 1980-2019, it was not because GDP shrunk). Now, if Levi was correct, lower profit rate countries should have smaller declines in the output-to-capital ratio, as the low profit rate should be an indication of a lack of opportunities to invest. And while it is true for a rapidly industrializing economy such as China versus the developed world, it isn’t true within the developed world itself. When we compare the US to Germany, France, or Japan, we see that the US has higher profit rates, but only a small decline in the output-to-capital ratio. The UK, for its part, had profit rates closer to those of developing China but output-to-capital changes equivalent to Germany, the country here with the lowest profit rate.

And here is precisely what I mean when I say that low investment rates experienced in the US and UK under neoliberalism are a choice. It was perfectly possible for other routes to be taken, as was shown by every other major capitalist economy.

I’ve touched on this previously in my exchange with Ted Reese, also in the Cosmonaut Letter’s section.

This structural role of the Chinese state is easy to differentiate from that of the US or UK, where all policy measures are taken to maximize capitalist consumption at the expense of all else, particularly investment. When I say that the UK’s crisis, which began with the great financial crisis and never ended was “avoidable” I mean that it was perfectly possible for the UK to have had a normal level of investment, given so many of its peers around the world were able to, even other countries with impeccable capitalist credentials. The US and UK are unique due to their role in capitalist imperialism; their level of de-industrialization was almost certainly so severe due to this structural role, which already in the years prior to World War 1 Lenin was calling out in the UK[: imperial surplus extraction cannot help but atrophy the domestic industrial base. The importance of US and UK financial sectors and other forms of rent seeking in the global economy mean they are the primary benefactors of such imperial surplus extraction. It’s in this way that the US and UK collapse in investment rates was avoidable, even from the perspective of its domestic bourgeoisie. Had the US and UK renounced and participated in the global economy primarily by selling actual commodities, their domestic bourgeoisie would have persisted, albeit looking a little leaner, and with the eventual risk of future falling profit rates leading to another crisis of capitalist reproduction. These discomforts and risks are things that the bourgeoisie of continental Europe, East Asia, and South America have simply lived with, after all.[2]

With regards to why the capitalists have made this choice, as, after all, many of the people holding these vast hoards of money capital have a fiduciary duty to expand it as much as possible, the answer is simple. Because fixed capital investment cannot be consumed by capitalists, it does not contribute to financial returns, which are essentially claims over flows of surplus that can actually be consumed. Fixed capital investment can produce big industries with big gross income amounts, where individual capitalists can “make up for a low margin with volume,” but why would capitalists choose to accept these additional costs when they can instead pursue financial or intellectual property rent seeking with their investments instead? As I’ve said before, even the fixed capital boom motivated by AI development was something of a bait-and-switch for investors who saw in AI first a software-based intellectual property play or the network effect associated with social media and search engines. This exorbitant privilege, however, is only really available to the Americans and the Brits to a lesser extent. Most countries need to export commodities to get access to the foreign currency needed to buy crucial supply chain inputs and consumption goods. In this way, the problem is too much opportunity for profitability rather than too little, and you’ll even hear capitalists talk often about just how much more dynamic the US economy is compared to Europe.

For the US, financial investment doesn’t necessarily translate into fixed capital investment for the reasons I originally pointed out in my essay, it can act as a capitalist but on a truly global level through the role its currency plays in international markets. Ordinarily, such low investment levels would lead to lower levels of real growth, something which would have alarmed both the government and the domestic capitalist class, but domestic consumption is able to be a source of growth so long as the commodities keep flowing in. Recent events may be quickly undermining such arrangements, however.

Liked it? Take a second to support Cosmonaut on Patreon! At Cosmonaut Magazine we strive to create a culture of open debate and discussion. Please write to us at submissions@cosmonautmag.com if you have any criticism or commentary you would like to have published in our letters section.

-

Basu, Deepankar, Julio Huato, Jesus Lara Jauregui, and Evan Wasner. 2022. “World Profit Rates, 1960–2019.” Review of Political Economy, November, 1–16. https://doi.org/10.1080/09538259.2022.2140007. ; https://dbasu.shinyapps.io/World-Profitability/

↩ -

Villarreal, Nicolas. “Letter: Truth from Facts.” Cosmonaut, 2026, cosmonautmag.com/2026/02/letter-truth-from-facts/.

↩