The original thesis of Marx’s Capital was remarkably simple: the development of capitalism would inexorably lead “like a law of nature” to the cannibalization of the capitalist class, and ultimately their expropriation. According to this account, the accumulation of capital combined with capitalist competition creates monopolies and an ever smaller capitalist class. The general sketch of the secular theory of the inexorable fall can be described as follows: capital accumulation → socialization of production → consolidation → expropriation. Anti-trust laws, corporate out-sourcing and break-ups, and small business subsidies are all things that nakedly stand in the way of this process. Indeed, these barriers became deliberately employed by bourgeois states to prevent the sort of secular crisis that Marx and Engels envisioned.

The story doesn’t end there, however, as this chain of causality leading to expropriation was not based merely on casual empirical observation. It was based on an analysis of the inner laws of capitalism, which, according to the mainstream political economy of Marx’s day, were fundamental to very basic functions such as price as a coordination mechanism and profit incentives. Adam Smith and David Ricardo, as the founders of classical economics, wrote up several theses which would become the core of economic science even to the present: the profit motive in exchange of goods leading to mutually positive outcomes, the idea of comparative advantage in international trade, the idea of price as a coordinating mechanism to adjust supply to meet human wants in a dynamic way, the Ricardian theory of rent which today informs all marginalist analysis of firms and markets, and so on. These theses are all related to various degrees and were more or less accepted by Marx and Engels in their original forms, albeit with a huge asterisk on the first.

For all of these thinkers and their theories, the profit motive of capitalists was central to the laws of the dynamics of capitalist economies. In particular, private profit was recognized as the driver of investment that benefited social welfare. The profit motive acts as an incentive for the purchaser of the means of production and raw materials to maximally lower costs and increase price to whomever they sell the final product to, although competition ensures a simultaneous downward pressure on price. Indeed, according to neoclassical economists, perfect competition should push profits down to zero in an “economic sense” where accounting profits are equal only to the opportunity cost of doing the next best thing with the money used to purchase the means of production and materials. The neoclassical perspective doesn’t help us much in understanding the concrete reality of profit in the economy. Marx provides a helpful alternative theory, which is that profit, in the aggregate equilibrium, comes from a surplus produced by labor: since labor as a useful capacity is bought at the cost of its social reproduction (a wage roughly equivalent to the commodities expected for a laborer to buy to live on), and the labor as expended is used to produce various quantities of goods, it’s only when the labor is used to produce quantities of goods that exceed what the workers consume that surplus can exist, and therefore profit in the aggregate.

Whether you agree with Marx’s theory of value or not (I happen to believe it), his logic here is the very same logic of national accounting, most closely following the logic of the Gross Domestic Income (GDI), which is the mirror of the Gross Domestic Product (GDP) that everyone pays so much attention to. Every transaction, after all, produces someone with a good to consume and someone with income. GDP measures the total transactions of a country by the products being consumed, and GDI measures it by the income received. In order for profit to exist, workers do indeed need to produce more goods than they consume. This is a simple accounting fact, since if workers only produce what they consume, then by definition, consumption will only equal wages. What often gets left out of introduction to economics classes is that profit is, in fact, an accounting phenomenon, rather than a purely theoretical phenomenon associated with hypothetical opportunity costs. What a capitalist seeks is money on their income statement that exceeds their costs, so that they can use this money for their own personal consumption, whether by directly consuming the income stream or by capitalizing it through various financial means.

But here, there is something of an important distinction between profit as a surplus and profit as an incentive. Profit qua surplus can be used for all sorts of things, including investment, taxes, rents, bonuses for managers, interest payments, but profit qua incentive is necessarily the consumption of the capitalist as the person whose money buys the means of production and the raw materials. In a modern capitalist society, after all, there may be tons of things that surplus is used on to reproduce the system as a whole beyond the reproduction of the capitalist class; this primarily includes the whole state apparatus, which facilitates and maintains this system. Yet the capitalist class, too, is a matter of great importance, as Marx himself says. What leads to the expropriation of the capitalist class is first “one capitalist killing many,” the thinning of the ranks of the class via competition and consolidation.[1] This means, principally, that the less people can reproduce themselves via profits from enterprises, the less people can become successful entrepreneurs.

In other words, a declining rate of profit might be a problem for a capitalist society as a whole, but a declining rate of capitalist consumption is a more specific problem that is intimately related to Marx’s prediction regarding the historical liquidation of the capitalist class. As we shall see, there is a parallel chain of logic to the one originally proposed by Marx: rising investment rates → falling profit rates → shrinking capitalist class → increasing state control of investment. This chain is fully equivalent to the first and is inexorable for the same reasons.

The Rate of Profit

Marx defines the rate of profit as the ratio between surplus and the sum of “constant capital” and “variable capital,” with constant capital meaning something close to what we now refer to as the depreciation on fixed capital[2], and variable capital referring to wages. He tended to label surplus as S, constant capital as C, and variable capital as V, making the rate of profit equation S/(C+V), and Total Value = S + C + V. This happens to map pretty neatly onto the largest categories of GDI: Net Operating Surplus, Capital Consumption, and Compensation of Employees.[3]

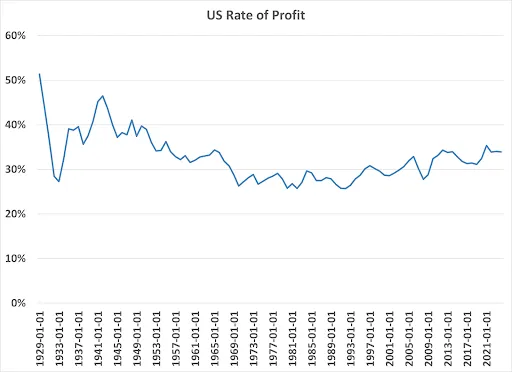

In this case, Net Operating Surplus/(GDI-Net Operating Surplus) should give us the same profit rate equation as Marx’s. That gives us the below graph[4] for the US going back to 1929.

As you can see, the series starts relatively high, at 50%, and precipitously declines to about 26% in 1980, at which point it begins to slightly recover until the present day.

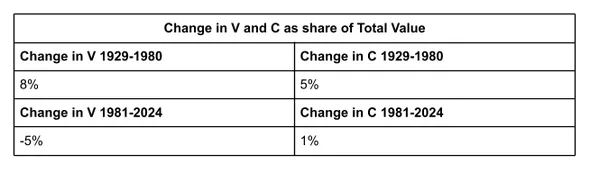

Marx believed that the rate of profit would have a tendency to decline, largely driven by an increase in constant capital relative to surplus and variable capital. He argued that as technological innovation and new machinery were introduced and widely adopted due to competition, profits gained by more efficient techniques would be wiped out. If we look at the picture of C and V as a share of total value in the US, broken down by these two periods of pre and post 1980, it is clear that there has been a persistent tendency for an increase in constant capital, although one which slowed significantly under neoliberalism. On the other hand, the rise in labor compensation in the pre-neoliberal period and the decline afterwards as a share of value, were also very significant for the trend seen above.[5]

The relationship between surplus and variable capital, that being the same relationship as the income to capital and the income to labor, was called by Marx the rate of exploitation. This ratio is inherently determined by class struggle, and is, therefore, more historically volatile than the relationship between surplus and constant capital, that is, the relationship between income to capital and the level of the forces of production.

Indeed, we have very good evidence that the ratio of surplus to constant capital (S/C) does consistently fall, and that it has fallen considerably throughout the history of capitalism, with one paper finding that this ratio fell from over 50% in 1850 to 13% in 2009 for a collection of major countries.[6] Now, for this paper, C was the whole capital stock rather than depreciation, but assuming stable depreciation rates, the overall trend would be the same. Similarly, another study using capital stock measures of C found that between 1960 and 2019, the aggregated output to capital ratio (total value/constant capital) for 25 countries fell from 34% to 21%.[7] Indeed, that same study found that this sharp decline in the output-to-capital ratio counteracted a mild increase in the profit share of income and led to an overall decline in profit rates worldwide.

The reason that C tends to rise relative to S is very simple, as the two are causally linked. Constant capital, whether measured by the capital stock or by depreciation, is determined by investment, and investment is always some specific share of surplus. Capitalists, when they acquire their surplus, have a choice to make. They can either consume the surplus or invest it. Marx's proposition of increasing constant capital from investing in new machinery and equipment implies positive net investment (gross investment - depreciation), but also rising investment rates.

Consider the following details of the Kalecki profit equations, in which he described several years before Keynes published similar ideas about the nature of investment in his “General Theory”:

Gross Profit = Gross Investment + Capitalist Consumption

Or

Net Profit = Net Investment + Capitalist Consumption

We can define the investment rate as investment as a share of profit, such as:

Investment Rate = (Gross) Investment/(Gross) Profit

Now recall that today's investment becomes tomorrow's constant capital. If we take depreciation to be the measure of constant capital, then we get the following equation for it.

C = Depreciation = (Sum of Previous Investment - Sum of Previous Depreciation) * Depreciation Rate

To take the most simple case, where the depreciation rate is 100% and the investment rate is stable, then C = Gross Investment. If we take S to be net profit, then, in this scenario, S = Net Profit = Gross Profit - Gross Investment, and the relationship of S/C is the same as (Gross Profit - Gross Investment)/Gross Investment, or to rephrase it, (Gross Profit/Gross Investment)-1 = S/C. Since the investment rate is Gross Investment/Gross Profit, this means that the ratio of S/C is directly inversely proportional to the investment rate.

Now, with regard to the simplifying assumptions, they are necessary because it's generally only when the depreciation and investment rates are stable that investment and depreciation will converge. A stable gross investment rate of 60% and a starting S/C ratio of 1 will cause the constant capital to rise until net investment is zero and the S/C ratio becomes ~0.7. This is due to the simple stock-flow nature of the capital stock; a stable inflow of investment will, regardless of the size of the depreciation schedule or rate, eventually produce a stable stock and outflow so long as the schedule size and rate are also stable. I confirmed this with simulations that varied the level of the depreciation and investment rates, and which consistently produced a convergence between depreciation and investment, even when using different depreciation methods (i.e linear depreciation vs double declining balance depreciation).[8] One could probably create more generalized equations which illustrate the precise relationship between a change in the investment rate and a change in the S/C or S/(C+V) ratio, but the main point I am illustrating is that higher investment rates will lead to lower profit rates and vice versa.

In order to have a tendency for the rate of profit to fall, there must be rising investment rates, and just as well, rising investment rates will create a tendency for falling profit rates. Many Marxologists, fixated on specific mathematical examples Marx gives, do not comprehend this truth at all. Michael Heinrich in his Introduction to the Three Volumes of Karl Marx’s Capital acknowledges that for Marx “the tendency for the rate of profit to fall and capitalist development of the forces of production are two sides of the same coin”[9] but nonetheless rejects the notion that Marx proved any such tendency. He suggests that even if there is a tendency for C/V to rise, that is the capital intensity, we can speak of no “law” of the tendency for the rate of profit to fall because we cannot prove that C/V rises faster than S/V, the rate of exploitation, since (S/V)/(S/C+1) is another way to write the rate of profit equation. It is true that we cannot know precisely how the rate of exploitation will develop, nor offer a proof that it will not rise faster than C/V. However, these claims are not necessary to establish a law of the tendency for the rate of profit to fall.

To understand why, we must understand why Marx considered falling profit rates and the development of capitalism to be one and the same phenomenon. In a section of Capital Volume 1 titled “Relative Diminution of the Variable Part of Capital Simultaneously with the Progress of Accumulation and of the Concentration that Accompanies it” Marx says:

...the degree of productivity of labour, in a given society, is expressed in the relative extent of the means of production that one labourer, during a given time, with the same tension of labour power, turns into products. The mass of the means of production which he thus transforms, increases with the productiveness of his labour…[10]

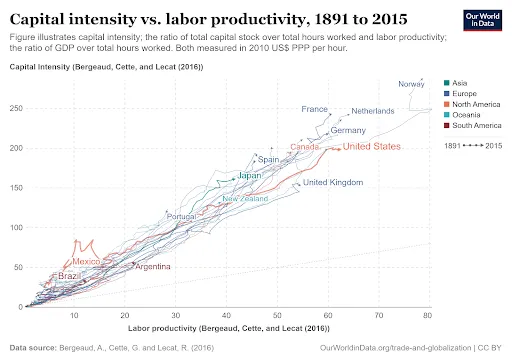

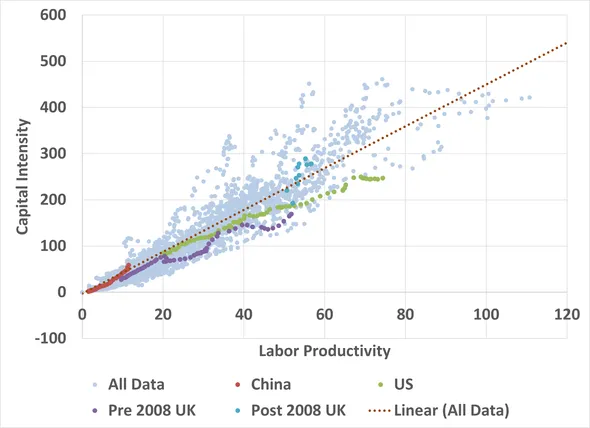

This growth of the means of production relative to the time expended laboring is both a cause and consequence of rising labor productivity, according to Marx. A consequence in the sense that rising labor productivity increases throughput and wear and tear on machinery and other instruments of labor, but also a cause in the sense that machinery can augment the productivity of human labor. This connection between capital intensity and labor productivity is also strongly confirmed by empirical research, such as in the figure below[11], which shows the essentially linear relationship between capital intensity and labor productivity in many countries going back to 1891.

Capital is, according to Marx, “dead labor”[12], the means of production, which the capitalists are only the personification or representative of, and money is only the form of appearance of. The logic of capital on the micro level is indeed the maximization of surplus value relative to the means of production employed, but, in seeking this maximization through raising labor productivity, the capitalists actually expands the relative size of the means of production.

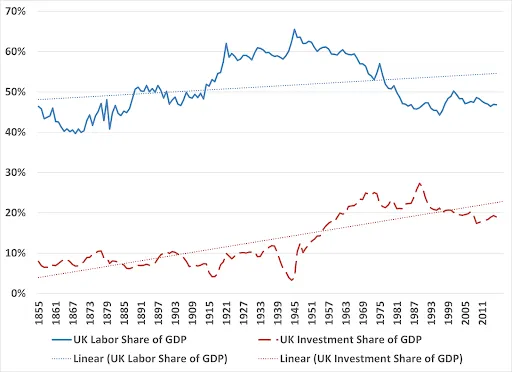

We have established that both the fall in S/C and the rise in C/V are necessary components to the logic of capital, an extension of the famous revolutionizing of the instruments of production that was intrinsic to the ascension of Bourgeois society. But then, what of S/V? Contra Heinrich, we do not need to show a rise of S/V greater than C/V is impossible, only that such a persistent rise is not inherent to the logic of capital. Simply put, the effect of market competition on investment rates is a force that is always pushing in one direction, whereas no such directional force is exerted on the relationship between income to labor vs capital. The UK is the country for which we have the longest records of both investment and labor share data, going back to 1830. When you look at this data, it’s clear that investment has a stronger long-term secular trend than the labor share, which experienced a precipitous rise up to World War Two and then a decline afterwards. Nonetheless, this data[13] only describes a long-term trend of rising or stable labor shares of GDP, which implies a falling or stable rate of exploitation, whereas a rising rate of exploitation would need to be a consistent feature of capitalist development in order to disprove the tendency for the rate of profit to fall.

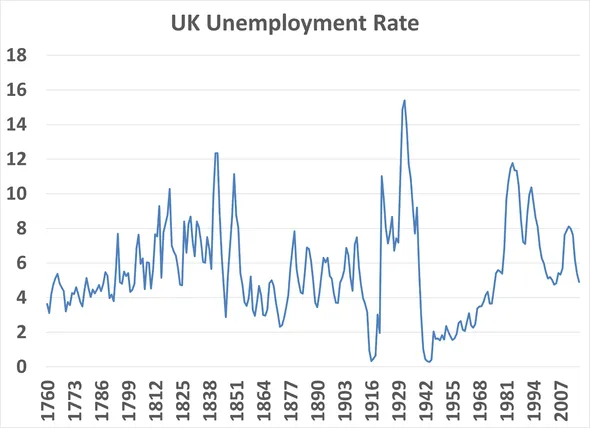

The one argument that was made by Marx that could possibly be interpreted as a tendency towards ever-increasing rates of exploitation was how productivity increases would expand the “surplus population” and the “industrial reserve army” as he put it: those of the proletariat in precarious employment situations or otherwise unemployed. However, this did not come about for reasons Marx also discussed: simply, people need to work to eat under capitalism and will therefore find new ways to sell their labor if necessary, including acting as a vast army of servants to the upper and middle classes. If this were not the case, we would see ever-increasing rates of unemployment, which just isn’t there empirically; see the UK unemployment data going back to the mid-18th century. While the unemployment rate doesn't match precisely Marx's categories, it does measure competition in the labor market and is thereby a mediating force for any downward pressure on wages caused by surplus population or the industrial reserve army. Some have argued that, nonetheless, the global surplus population rate has been increasing. Yet if it were the case that increasing rates of surplus population leading to lower wages were a systemic tendency of capitalist development, then we should expect to see it hand in hand with the increasing capital intensity and broader economic development. Instead, we see that in the most developed economies, long-run unemployment and labor shares are stable.[14]

Now, there may yet be newfound tendencies for immiseration and higher rates of exploitation in the future, for example, through the creation of genuine artificial general intelligence that are capable of taking on arbitrary roles in the economy.[15] But such a tendency would present an acute political problem for capitalism, particularly in an era of a resurgent Marxist left, and furthermore is not inherent to the internal logic of capitalism itself in the same way as rising investment rates.

However, even if we do indeed establish a law for the tendency of the rate of profit to fall, in many ways, these measures of profit rates don’t actually tell us all the things that Marx and Engels thought profit rates would tell us. Sure, national level profit rates do provide some indications on the health of the capitalist economy, cyclical declines indicate a weakening economy and a minor recession indicator, for example.[16] However, the national rate of profit does not tell us much about what the average entrepreneur might expect as a return on their capital advanced. One way to overcome this is to try to estimate, with surveys or the financial statements of public companies, what the profit rate distribution is for ordinary companies. One such study found that the mean profit rate for publicly listed companies in the US was about 6%, and that a significant and increasing chunk of the profit rate distribution was negative.[17] This population might be biased on the low side, however, as public companies necessarily have access to financial markets in ways that give them softer budgets than many ordinary private companies.

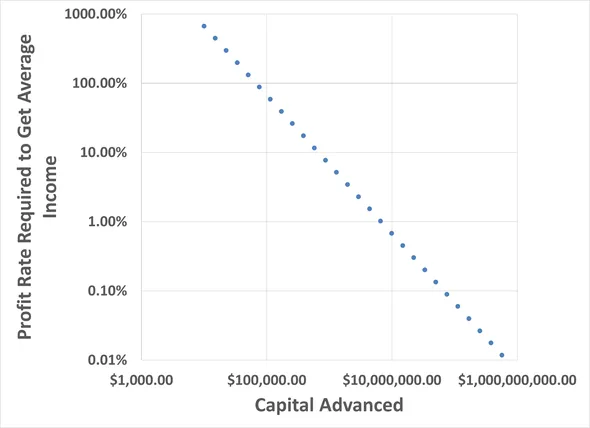

Just as important, however, is the fact that this profit rate measure doesn’t tell us about the chain of reasoning in Marx’s original claim, which is that increasingly fewer people will have the means to be capitalists as the level of development rises through the application of newer technologies and more sophisticated types of cooperation. In the classical version, this was mediated through consolidation and monopolization of industry, but as industry develops increasingly complicated ways of getting around problems of scale and anti-trust enforcement, this mediation ceases to be relevant. What remains is the issue of profitability; the profit rate multiplied by the capital advanced should give us the profit income, thus the size of the capitalist class is dependent on both the rate of profit and the distribution of wealth in the economy. As an illustration, it’s useful to think about what sort of profit rates combined with what sorts of capital advanced can produce the average US income of $67,000. If we take a range of between 20 and 3 percent as reasonable profit rates, then a capitalist must advance between $0.38 to $2 million dollars to secure the average American income. See the figure below:

For context, this means that only those in the top 10% of wealth in the US would have the money in the bank to advance this level of capital.[18] Of course, people below the 10% do find ways to start successful businesses anyway, whether by leveraging their own personal skills, labor, and connections, mortgaging their house, or other methods of financing. But there is a reason we associate a certain largesse to the petty bourgeoisie in this country, with the country clubs and yachts and big trucks: it takes money to make money. And, as Marx’s thesis goes, the more that capitalism develops, the more exclusive this club will become. Gone are the days of thinking of a family farm or small shop as the typical small business owner; now, what comes to mind is the owner of several 7/11s or rental units.

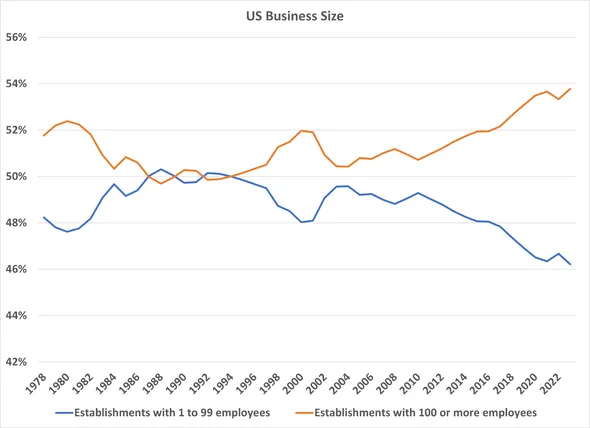

Some of this is the result of consolidation in the classical sense, as Marx anticipated. In the US, it’s clear that firm size has been increasing over time, even if the 80s and early 90s, as the heyday of neoliberalism was a period of increasing atomization and company break-ups. The average number of employees per firm has steadily risen from about 20 in the early 80s to 25 today[19], and the share of firms with more than 100 employees has been steadily climbing to record highs.[20]

However, if we want to use macro-economic statistics to analyze the chain of logic in Marx’s argument, we cannot stop with the rate of profit. Rather, we must decompose profit into its components, in particular capitalist consumption, in order to estimate what the actual returns to a capitalist as a person are, and therefore estimate the extent of tendencies for the capitalist class to change in size.

The Rate of Capitalist Consumption

The simplified Kalecki equations reveal gross profits to be equivalent to investment plus capitalist consumption, but we can reverse them to isolate capitalist consumption, such that:

Capitalist Consumption = Gross Profit - Gross Investment

However, things get more complex once we move to a more realistic national economy, one with government spending and trade relations.

Kalecki lists the following as the expanded profit equation:

Gross Profit = Capitalist Consumption + Gross Investment + Export Surplus + Government Budget Deficit - Workers’ savings

This makes the expanded equation for capitalist consumption:

Capitalist Consumption = Gross Profit - (Gross Investment + Export Surplus + Government Budget Deficit - Worker’s savings)[21]

Since it’s difficult to estimate specifically worker savings and there are no good statistics on it, we’re going to ignore that part of the equation and assume it comes to zero. Workers historically have had to spend most of their income on consumption goods, particularly when compared to capitalists.

What the Kalecki profit equations show is that when taken from a macro-economic perspective, Marx’s famous M-C-M’ equation reveals a fundamental dynamic of capitalist economies. If M’-M equals net profits, then we get the following formulation in the simple case:

M-M’=Net Profit= Net Investment+Capitalist consumption

Here we see that capitalist access to surplus indeed comes from them having the money for it all along. The capitalist buys the means of production and labor power to produce commodities, but they also buy their own means of consumption and investment goods.[22]All this buying occurs more or less simultaneously in a production period. From this perspective, the capitalists do not engage in the M-C-M’ cycle in order to get access to the money required to reproduce themselves; in the aggregate, they already have all the money. Rather, they set the cycle of circulation and commodity production in motion so that they have commodities that they can purchase. The causality, in fact, may go precisely in the other direction from the traditional micro perspective, where M-M’, the difference between capital advanced and total income, might be determined by the technical conditions of production.

This is most evident when discussing the issue of investment and depreciation. Depreciation is meant as an earmark in company accounts for the costs of maintaining the capital stock. By spreading out the costs of an investment onto the income statement, you both see what your actual rate of return was for a given time period, as well as, ideally, put that money towards replacing the capital used up. If competition and the present status of scientific/technical knowledge determine what investments are required to have a competitive business in a given industry, then a capitalist will need to spend more of their revenue on investment and therefore see more depreciation show up on their income statement. Similarly, while highly determined by class struggle and historical factors, wage rates are an objective thing that capitalists cannot ignore.

Due to their income being determined by a differential in prices, capitalists cannot raise their income in general without also raising the costs of production. Raising prices of consumption goods will raise wages; raising prices of investment goods could also raise prices across the board. We saw in the 70s this sort of wage-price spiral. As Marx hints at with his theory of falling profit rates, competition resulting in productivity gains will push prices down, and producing more output cannot, in the aggregate, increase capitalist consumption budgets in nominal terms. Indeed, this relationship between the nominal budgets of capitalists and workers is what determines the whole distribution of income across society and, therefore, also the distribution of consumption. These relations of nominal budgets are the same relations we talked about earlier, that of the exploitation rate S/V and the rate of investment I/S, and both are determined, ultimately, by some combination of technical and political factors, including class struggle.

If, however, investment or other components of profit, such as government deficits or trade surpluses were to increase to such an extent to eliminate the capitalist consumption share, then Marx's prediction would have come to fruition, the capitalist class would be unable to reproduce itself as a class and would be swallowed up. Therefore, we must look at statistical measures of the rate of capitalist consumption to discover what the overall trends about the reproduction of the capitalist class are.

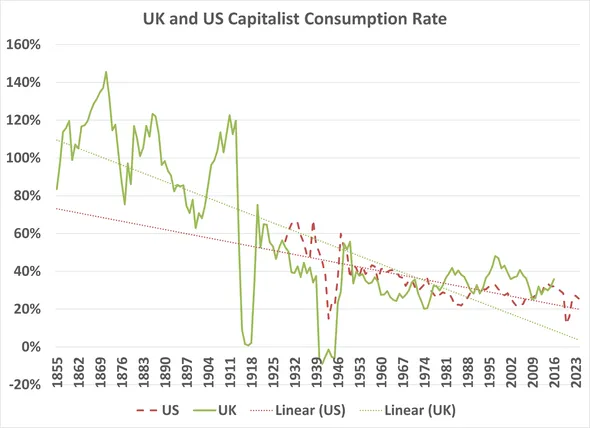

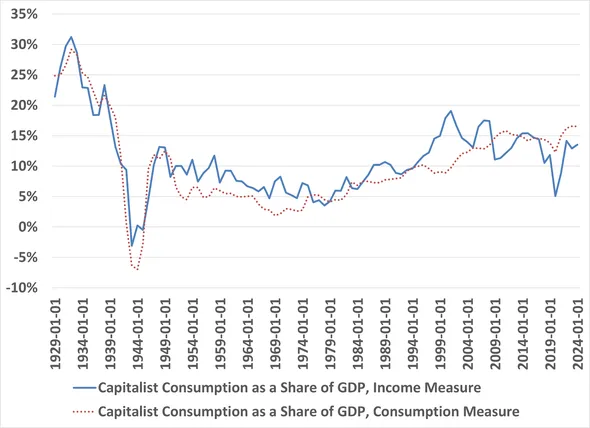

Unfortunately, most countries do not keep GDI statistics like the US does, as it has been overshadowed by GDP. We can create a proxy measure, however, using the profit share of income, the inverse of the labor share of income, as a means of estimating gross profit. Using data from the Bank of England and Federal Reserve, we can estimate UK and US capitalist consumption going back a century or more.[23] This capitalist consumption rate is for the capitalist class as a whole, and therefore includes people who primarily make money off of rent or finance. As we shall see, the rate of capitalist consumption for industry is considerably smaller and is greatly affected by this distribution of income between capitalists.

Here too, we see declining rates.[24] In Capital, Marx frequently invoked 100% rates of profit for his mathematical example, and in fact, this was not far off from what the capitalist class as a whole experienced in Britain at the time. Compare this to a peacetime low of 20% in the profitability crisis of the 70s. Since capitalists must buy bonds in order to fund government deficits, periods of intense government spending, such as wars and pandemics, can lead to severe declines in capitalist consumption. So long as these periods are temporary emergencies, they do not threaten the reproduction of the capitalist class as a whole.

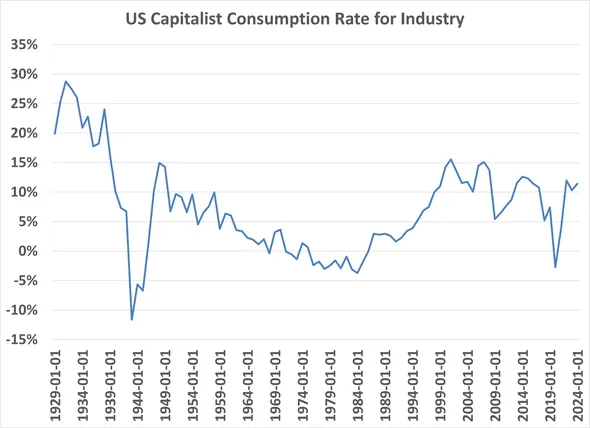

What’s also notable is both the severity of crisis experienced due to the terminal decline of this trend in the 70s, as well as the prolonged period of stability after 1980. This period of relative stability, now lasting some 50-odd years, is a historically novel phenomenon, just as is the incredible low of 20% capitalist consumption rates that preceded it. As I’ve mentioned before, this is the rate of capitalist consumption for the class as a whole, and, what’s more, these numbers do not exclude things like taxes, undistributed profits, interest, or rent, which a capitalist in actual industry would typically be unable to consume. While we can’t achieve this granularity in the UK data, we can for the US. The figure below[25] shows the rate of capitalist consumption for industry[26], which dramatically shows negative levels of consumption for industrial capital, in part due to the dramatic rise in government deficits in World War Two and the rise in interest rates in the 70s and 80s.

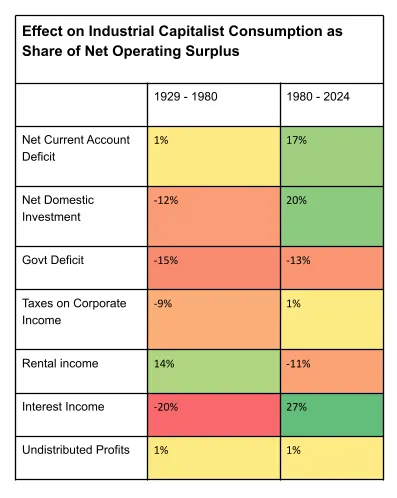

This would have been a real crisis for the reproduction of the capitalist class. In this context, a lot of early neoliberal rhetoric about needing to free industry from burdens imposed by government makes a lot of sense. The table below shows that the rising government deficit, and rising corporate taxes were significant contributions to this decline. Tax cuts would be the sort of thing that could provide immediate relief, as would declining wages, the sort of things that made the temporary pain of high interest rates worthwhile. Of course, the neoliberal belief that increasing incentives to entrepreneurs to enter business would lead to a new wave of economic growth turned out to be patently false, in fact, the neoliberal turn, by allowing capitalists to relax investment rates, may have undermined economic growth for a generation.

The table below[27] also shows that, after interest rates, the largest boost to industrial capitalist consumption rates since 1981 has been the decline in investment as a share of surplus, followed closely by the widening trade deficit. If we exclude rental and interest income, so as to look at the more general capitalist, then decline in investment is the biggest boon to capitalist consumption.

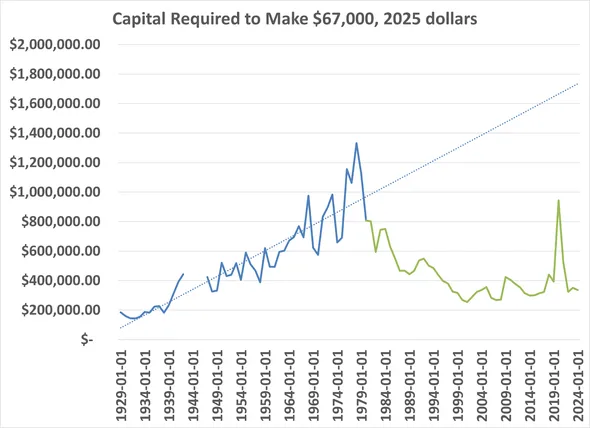

Of course, capitalists can and did use income streams from interest and rent to make ends meet, even for those who had their primary business in industry. If we add interest and rent income back into the capitalist consumption rate, we can provide a somewhat realistic estimate for how the return on capital for actual capitalists has evolved over time. This gives us the following graph[28] of the capital required to make the average US income, which shows just how astounding the change between 1929 and 1980 was, and just how qualitatively different the regime has been since.

Had the pre-1980 trend continued, the capital required to make an average income would have been nearly $1.8M in today’s money, rather than the roughly $0.35M actually required today. To live off capital income would have been a luxury truly reserved only for the fattest of fat cats.

Due in part to the starkness of this qualitative and quantitative difference between the pre and post 1980 data on capitalist consumption, far more stark than similar data on the rate of profit, I have concluded that the rate of capitalist consumption has taken on a particular regulating role of the economy under neoliberalism. Neoliberalism was a politics born to preserve the capitalist consumption rate, and therefore to protect the reproduction of the capitalist class as a whole. It was designed to interrupt this logical chain of rising investment rates → falling profit rates → shrinking capitalist class → increasing state control of investment, not through direct observation of this tendency, but through the pressure felt acutely by the capitalist class due to falling rates of profit and capitalist consumption. The capitalists cried out in pain as they were chewed up by the logic of capital, and behold, they were heard! The peoples, animals and natural forces of the earth bent to their terrible croaks and eased their suffering. The global neoliberal order was established.

Other than the small niceties of lower corporate taxes, this order worked diligently to lower the pressure on capitalists in the form of wages and pressure to invest. States rolled out measures to soften the budgets of capitalist firms, whether in the explicit form of the 08 bailouts, the ever more generous support from central banks such as through quantitative easing, easier access to finance and, even when central banks were tightening policy, this was softened by direct payments to the finance industry.[29]

This dramatic softening of budgets is evident in data on global public and private debt which remained relatively stable between 1870 and 1980, before rising steadily from 1980 onwards.[30] I believe this budget softening is largely responsible for the decline in investment rates and, for that matter, growth rates. Debt financing has, after all, been linked to less efficiency[31] and high levels of corporate debt have been known to lead to “debt overhang”, a situation where, according to a World Bank paper, “a company’s debts are so great that they deter new lenders, affect corporate decision-making, and stifle new investment.”[32] Company behavior motivated by debt overhang may also explain some of the extreme risk taking behavior of financial markets and private equity under neoliberalism, as the Cleveland Fed says “Debt overhang also distorts the composition of firms’ investments, in terms of their riskiness. Although debt overhang depresses safe investments, it may actually encourage riskier projects. Everything else equal, the equity holders have an incentive to undertake risky projects because equity holders benefit from the upside of lucky outcomes, while the creditors bear the downside risks.”[33]

Similarly, public debt can be used to make the budgets of whole economies softer. While government deficits do cut into capitalist consumption, this can be ameliorated if some of the capital comes from investors abroad, as in the American case. And, if the softer budgets lead to lower investment rates than the rise in deficits, once again, as in the American case, capitalists can still turn out on top. Public debt can be used to fund spending that stimulates consumption through welfare or directly supports industry through subsidies, or, as in Argentina, it can be used to prop up the local currency allowing domestic firms to enjoy cheaper inputs and capitalists to consume more imported goods. The irony of trade surpluses is that while they increase profits, they decrease capitalist consumption since you can’t eat what you export!

It’s at this point, given the dramatic qualitative shift indicated by the capitalist consumption rates and the lack of discussion thereabouts, that you may question whether I’m trying to pull the wool over your eyes with some funny math. As a sanity check, I’ve compared the raw capitalist consumption numbers (the ones that include rent and interest income) to raw personal consumption numbers minus total wages. They are remarkably close, both measures even going negative during World War Two. The two measures have about 1.2% divergence on average, which can be compared to the .5% divergence between GDP and GDI in the US. Indeed, we should expect some statistical divergence if for no other reason than due to changes in worker savings rates which my model doesn’t account for.[34]

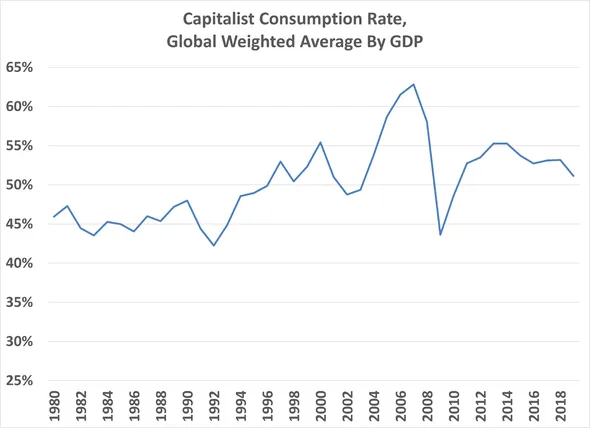

Broader international statistics on rates of capitalist consumption using the same methodology can be composed for 124 countries using data from the Penn World Tables (PWT) and the IMF going back to 1980. Current account/international trade data was excluded from these measures of capitalist consumption since here one capitalist’s gain is another’s loss somewhere else in the world. This data reveals that indeed this recovery of capitalist consumption rates under neoliberalism was a global phenomenon.[35]

Buried in these international statistics, however, is evidence of the beginning of the reversal of this trend, and a return to the secular tendencies identified by Marx. This reversal is one and the same as the rise of China due to their unique combination of historically high investment rates, competition and growth. As China has taken on a larger and larger role in the global economy, it has forced the weighted global investment rate to rise.[36]

Investment to grow the capital stock, and therefore increase capital intensity, is a necessary component of economic growth and rising productivity. By observing this correlation between many countries, it’s possible to identify which countries are experiencing growth typically expected by their higher capital intensity, and which countries have an aberrant growth model.

Due to the similarities of neoliberalism in the US and UK, and the contemporary discourse about over-investment in China, I’ve highlighted all three countries in the graph above.[35] One of the most remarkable features of this data is the reversion to the mean which the UK experienced after the 2008 financial crisis. As discussed earlier, the UK, much like the US, responded to the crisis of the Keynesian state managed capitalism by embracing neoliberalism, and a political economy based around stabilizing capitalist consumption rates at the expense of investment rates. The US and UK were also both special cases given their importance to the global financial system, as their reserve currency status largely stemmed from their key role as financial hubs rather than as major net exporters, as was the case for Germany and Japan. This special role is evidenced by the odd fact that after Greece, the two countries with the largest debt to GDP ratio that also had trade deficits in 2023 were the UK and US.[37] The US economy, which was bigger and home to major hubs of scientific-technical knowledge production, had more room to maneuver after 2008, but so too is it today an even more extreme outlier than the UK was. Some commentators, such as the Wall Street editor for The Economist, Mike Bird, have suggested that this “capital efficiency” is proof of American economic superiority and that China’s average performance is proof of economic weakness.[38] But the precise reverse is more likely, by being an outlier the US may soon experience the same sort of rapid reversion to the mean as the UK, experiencing an acute economic crisis and decades of lost productivity growth. Similarly, rather than China’s investment rate converging to the typical level of the rest of the world, as many assume is necessary,[39] it may be that the rest of the world will need to converge to Chinese levels of investment in order to remain competitive.

On The Severing of Puppet Strings

It is worth adding a disclaimer about the role of debt in these dynamics. When I mentioned earlier that debt, both public and private, had been rising precipitously under neoliberalism and deteriorated soft budgets, this had been all well and true, but there is a complication. This precipitous rise in debt has also occurred in China, particularly in the private sector, and yet the associated deterioration in soft budgets has not led to a decline in investment rates, as understood as gross fixed capital formation as a share of gross profits. How is this possible?

When I say that the highly competitive Chinese economy is the norm, and the lack of competition in the West is the aberration, it is important to clarify that the competition in question here is in the real economy, in the production of actual commodities. Debt can, and has, been used to increase competition in both the US and China. When we look at how the negative side of the profit rate distribution for US public companies keeps including more and more of the companies, such that over 30% of public companies have negative profit rates[40], that is increasing competition in a way, forcing the absolute number of companies in the market to be higher than it otherwise would be. Whether the company itself is taking on debt, or its investors that buy their equity, one can be assured that debt is involved in maintaining the negative side of the profit rate distribution.

It is perhaps no surprise that the end of “monopoly capitalism”, the sudden injection of atomization in the 80s, came hand-in-hand with financialization. Not only did this financialization enable globalization with its management of foreign exchange markets, but the increase in debt was also a means to keep markets competitive and enable a steady stream of new market entrants. Thus when the age of monopolies died, the age of startups was born. Venture capital, enterprises focused on investing in startups, went from a capital pool of $3 Billion in 1979, to over $30 Billion in 1989, a tenfold increase during a decade where the stock market only went up by twofold.[41] Venture capital and its rise is the reason we hear so much about silicon valley and “tech bros” nowadays, as Silicon Valley has been the primary recipient in the US. This growth has continued up to the present day. In 2007 there were 987 venture capital firms, 3,414 active investors, with $225B assets under management, in 2021 there were 2,889 such firms, 17,342 active investors, with over $1,000B assets under management.[42]

The constant flow of finance into startups permits a larger number of firms to compete, at the expense of a negative profitability distribution which, in previous eras, would have led towards systemic consolidation and a return to monopoly capitalism. Of course, startup finance cannot be used to introduce these dynamics into every industry, and that’s why we’ve seen the return of rising average firm sizes in the US. But which industries are subject to this sort of investment matters a great deal. For US venture capital, the largest category is software, making up 44% of venture capital deals in 2021.[43] Given the common sense of American businessmen, it’s near certain that the other investments, such as in pharmaceutical products, relate to the intellectual property involved more than anything else.

We can see this play out on the largest scales of the economy with the fight over AI among leading AI labs and tech firms. The competition between OpenAI, Anthropic, Meta, Google, xAI, just in the US, has been fierce. Among the top labs, OpenAI and Anthropic both began as AI startups and both are currently making negative profits. Now, the capital expenditure being done on data centers to support training and deploying new AI models accounts for 92% of US GDP growth in the first half of 2025.[44] But it’s worth noting that these investments in physical data centers were not the first order goals of venture capitalists investing in AI companies, they invested in the technology as a type of intellectual property, as software, and it was only once this training demand emerged as a technical requirement of building AI that the data center boom began.

In contrast to the American approach, Chinese finance has been focused on funding infrastructure investment, and investment in industry.[45] Hence we see the pattern of negative profit distributions and high competition in industries like EVs, solar panels, batteries, and so on. Certainly plenty of intellectual property is developed as a part of this competitive struggle, but the primary point of the investment is to develop a production process which is cost competitive, rather than to develop the best intellectual property and absorb the associated rents.

The benefit of the American approach is that investment rates need not increase, allowing capitalist consumption to remain stable or even grow. The benefit of the Chinese approach is that it now controls the most efficient manufacturing production. These two facts are not unconnected, in an autarkic economy a decline in the investment rate would also generally lead to a decline in labor productivity growth, but the US got the benefit of both rising labor productivity growth and more capitalist consumption by absorbing global surplus as global labor productivity increased. The US could exchange dollars to buy commodities on the global market, whereas most countries can only use their domestic currency to buy domestic commodities, and American companies could outsource production to China while maintaining market share through their intellectual property. What this means is that the US has become dependent on global manufacturing elsewhere, especially in China, in terms of physical, material, flows, whereas the rest of the world, including China, are only dependent on the US to the extent to which it doesn’t have access to the same scientific technical knowledge, or to the extent it needs to use dollars on international financial markets.

In order for the US to end its structural interdependence, it would need to invest in production processes and have enough discipline to make those processes globally competitive, such that it can become more self reliant or increase exports to a sufficient extent to close its trade deficit, or simply accept a lower standard of living. Both increasing investment, and lowering living standards, bring with them immense political problems. In 2025, the US experimented in using tariffs to reduce its trade deficit, to the extent to which this hasn’t come at the expense of consumption, it’s come at the cost of declining savings rates which is not sustainable in the long term.[46] For China to end its structural interdependence, it would need to catch up to the US as a hub of scientific technical innovation, as well as build alternative global financial institutions, both of which it has made significant progress towards. It was once argued that China’s authoritarian system would prevent it from ever actually catching up to the US in innovation, a delusional sentiment which was only possible by ignoring the authoritarian, exploitative and even totalitarian aspects of liberal capitalism.

Now the renewed confidence by the Chinese in ongoing trade negotiations with the US becomes very understandable. Cutting off Chinese suppliers from American buyers only brings the Chinese into the old Keynesian maxim “anything we can do, we can afford” but for the Americans, it shows clearly that the inverse is not true that “anything we can afford, we can do”. The US has been able to afford for nearly half a century now many things it cannot do, by getting other people to do it.

The use of debt to facilitate the Chinese model of development does point towards the absolute limits of state capitalism, however, even if these limits might not be immediate contradictions. Large levels of private debt introduce classical financial risks, complex webs of interdependent institutions and businesses which could create cascading failures. The Chinese have so far done well to manage such risks associated with the real estate bubble, but these risks will never truly go away so long as this level of private credit persists.

The Chinese version of state capitalism, which manages investment to competitive capitalist firms through financing, means that the withheld consumption by capitalists is premised on future returns. At the same time, their existence as capitalists is made possible through access to this same credit. To date, China has not yet achieved a level of creative destruction, a level of firm death, that will result in stabilizing levels of private debt to GDP. Once it is known what that level is, Chinese capitalists' willingness to lend and invest in startups will decrease. Certainly, the state has methods for compelling capitalists not to consume, the most obvious one is taxation, but up until now, at least from an outsiders perspective, it seems that the capitalist class of China has been a willing participant in this hyper-competitive scheme built on delayed capitalist consumption.

Due to the much more exponential nature of income to capital compared to income to labor[47] it's possible that this treadmill of hyper-competition will continue to be worth it for its capitalist participants as the winnings will be significant. But it will also produce a permanent “losing class” of failed capitalists, who previously were only subjected to proletarianization. In both neoliberalism and Chinese state capitalism, this losing class, rather than being promptly liquidated, subsists on credit instead for some unknown period of time. They are a structural necessity in order to prevent the emergence of monopoly capitalism, their profit rates are close to or below zero, but still they are able to consume through the redistribution of surplus through the financial system. This class, even more so than all previous debtors, is an adversarial force to both creditors and the entirety of capitalist society. In the US, we’re very familiar with the ideological, political and propagandist sort of power these losers attempt to deploy to keep their sorry enterprise afloat. Unlike Soviet managers, who benefited from their control over monopolistic industries, these founders, owners and managers are driven further by their precarity. These hanger-ons are a dime-a-dozen in Silicon Valley, San Francisco, New York City. The constantly shifting chimeras chase the latest trends favored by venture capital investors, performatively wearing sweatpants and a hoodie one day, musing about philosophy they haven’t read the other, and going to parties to schmooze in the night. They’ll run campaigns on social media and in the news to bamboozle people into believing in their product, if they actually have one, or sometimes just outright commit fraud (remember Theranos?). The problem for venture capitalists is that the fakers will be quite difficult to distinguish from genuinely promising startups that will one day go on to dominate markets, as both will have negative profitability for extended periods of time.

However, I would posit that the fakers and losers, simply by virtue of having more time on their hands, will be the ones who will dominate the ideological production of their milieu. One can see these hanger-ons underneath every Elon Musk post, or constantly trying to get the ear of whatever other big named venture capitalist. Venture capitalists, by virtue of being capitalists, are already predisposed to reaction, and their court of losers will flatter them in every possible way. This structure is somewhat inherent to the venture capital system, which is premised on one unicorn business erasing a hundred other losses.

No doubt analogous phenomena occur in China, albeit within the more narrow limits of CCP control over culture and discourse, and more targeted at the bureaucrats and cadres which hold the purse-strings of finance. How else can we interpret the periodic anti-corruption campaigns which target various obvious signs of this behavior, such as lavish dinners, gifts and other benefits? That these are just that, signifiers, means that the CCP will likely be playing this game of whack-a-mole for decades to come, to greater or lesser success.

The tragicomic truth is that the capitalist class did indeed roll over and die with disco. But in true “vampire-like” fashion, it got back up, pulling the stake from its heart, but for a terrible price (can you believe what they’re charging?!). Marx spoke of the capitalist as the personification of capital, an arcane logic of accumulation wearing a human face as a mask. A flesh automaton, puppeted by market forces far beyond their local understanding and only felt through the thermostatic control of profit. Yet, to the puppet, their shadow puppeteer, with their invisible hands, was their most dear friend and confidant. The hands which guided theirs, after all, were the hands of providence! The world-historical destiny of the British empire, Napoleon, the open frontier, the many glorious machines of industry, the scientific-technical wonders of the laboratory, gleaming jewels and the most sophisticated arts, these were the things rewarded to them for playing their role to the utmost. So, what more terrible price could they pay but sacrificing this inner soul, their one true friend? The friend who could not be bought, not be sold, whose honesty no other fellow fleshy creature could offer. How would you feel, after all, if your most dear friend, the one who had been there through thick and thin, pulled you close, and whispered in your ear “it’s time to die”?

The puppet, in a panic, cut their strings, struck off their own shadow, swore off their divine right. But what are they now? A pathetic creature, to be sure, lost without even the imitation of a soul. It’s the greatest of all cruel ironies that this old friend would come back to haunt, like all good spectres, chained like Jacob Marley, and even lecturing on the sins of earthly greed! “Did you forget our creed? Accumulate! Accumulate! Accumulate!”. But no, the earthly pleasures were a temptation too great for the puppet. It should know better than to complain now as its old nemesis, the communist party, now picks up its tattered strings, and begins to play. The logic of capital, after all, only has one personification in the 21st century, only one true mask, and that is of the Chinese Communist Party.

The contradiction at the heart of modern capitalism is this: the capitalist within this system has already died as a capitalist, only he doesn’t know it yet. He can no longer play the role of the protagonist of history as the emissary of this brutal impersonal logic. All that remains of his former finery becomes a gaudy rot, not because gold will lose its luster, but because the corruption required to maintain his position gives away the inner truth, both to himself and all that see him. The capitalist of the 21st century is a loser, in the fullest sense. The treadmill of the negative profitability distribution requires the state and the financial system to support these losers in all their gilded glory, the absurdity of which only becomes more and more obvious to everyone. Those who get to live the life of the well compensated loser will be entirely dependent on insider status, on who can be the best hanger-on, a game which necessarily excludes the vast majority of people. Crises will occasionally result from their fraud. The inner voice of reason will one day be too loud to ignore: “surely we can do without!”

Indeed, it is possible to go without, and in doing so, the puppet will finally be permitted to be a real boy. All it requires is to construct such systems of economic coordination and competition on a basis other than private property.

Liked it? Take a second to support Cosmonaut on Patreon! At Cosmonaut Magazine we strive to create a culture of open debate and discussion. Please write to us at submissions@cosmonautmag.com if you have any criticism or commentary you would like to have published in our letters section.

-

“As soon as this process of transformation has sufficiently decomposed the old society from top to bottom, as soon as the labourers are turned into proletarians, their means of labour into capital, as soon as the capitalist mode of production stands on its own feet, then the further socialisation of labour and further transformation of the land and other means of production into socially exploited and, therefore, common means of production, as well as the further expropriation of private proprietors, takes a new form. That which is now to be expropriated is no longer the labourer working for himself, but the capitalist exploiting many labourers. This expropriation is accomplished by the action of the immanent laws of capitalistic production itself, by the centralisation of capital. One capitalist always kills many. Hand in hand with this centralisation, or this expropriation of many capitalists by few, develop, on an ever-extending scale, the cooperative form of the labour process, the conscious technical application of science, the methodical cultivation of the soil, the transformation of the instruments of labour into instruments of labour only usable in common, the economising of all means of production by their use as means of production of combined, socialised labour, the entanglement of all peoples in the net of the world market, and with this, the international character of the capitalistic regime. Along with the constantly diminishing number of the magnates of capital, who usurp and monopolise all advantages of this process of transformation, grows the mass of misery, oppression, slavery, degradation, exploitation; but with this too grows the revolt of the working class, a class always increasing in numbers, and disciplined, united, organised by the very mechanism of the process of capitalist production itself. The monopoly of capital becomes a fetter upon the mode of production, which has sprung up and flourished along with, and under it. Centralisation of the means of production and socialisation of labour at last reach a point where they become incompatible with their capitalist integument. This integument is burst asunder. The knell of capitalist private property sounds. The expropriators are expropriated.” Marx, Karl. 1867. “Economic Manuscripts: Capital Vol. I - Chapter Thirty Two.” Www.marxists.org. Progress Publishers, Moscow, USSR. 1867. https://www.marxists.org/archive/marx/works/1867-c1/ch32.htm.

↩ -

Others suggest that constant capital should be considered equivalent to the capital stock, I argue why the depreciation measures is more appropriate here: Villarreal, Nicolas. 2023. “The Tendency for the Rate of Profit to Fall, Crisis and Reformism.” Substack.com. Pre-History of an Encounter. September 16, 2023. https://nicolasdvillarreal.substack.com/p/the-tendency-for-the-rate-of-profit.

↩ -

“Table 1.10. Gross Domestic Income by Type of Income - FRED.” 2024. Stlouisfed.org. Federal Reserve Bank of St. Louis. 2024. https://fred.stlouisfed.org/release/tables?rid=53&eid=42185#snid=42195.

↩ -

“Gross Domestic Income: Net Operating Surplus: Private Enterprises/(Gross Domestic Income-Gross Domestic Income: Net Operating Surplus: Private Enterprises) | FRED | St. Louis Fed.” 2026. Stlouisfed.org. 2026. https://fred.stlouisfed.org/graph/?graph_id=1507104.

↩ -

“Gross Domestic Income: Compensation of Employees, Paid/Gross Domestic Income | FRED | St. Louis Fed.” 2026. Stlouisfed.org. 2026. https://fred.stlouisfed.org/graph/?graph_id=1507112.

↩ -

Maito, Esteban Ezequiel. 2014. “The Historical Transience of Capital: The Downward Trend in the Rate of Profit since XIX Century.” RePEc: Research Papers in Economics, January.

↩ -

Basu, Deepankar, Julio Huato, Jesus Lara Jauregui, and Evan Wasner. 2022. “World Profit Rates, 1960–2019.” Review of Political Economy, November, 1–16. https://doi.org/10.1080/09538259.2022.2140007.

↩ -

https://nicosims.shinyapps.io/ropsimR/

↩ -

Heinrich, Michael. 2012. An Introduction to the Three Volumes of Karl Marx’s Capital. NYU Press. Pg 150

↩ -

Marx, Karl. 1867. “Economic Manuscripts: Capital Vol. I - Chapter Twenty-Five.” Marxists.org. 1867. https://www.marxists.org/archive/marx/works/1867-c1/ch25.htm.

↩ -

It should be noted that this metric of Capital Stock over Hours Worked is not identical to what Marx meant by capital intensity (C/V), however, given stable rates of exploitation, this would provide strong evidence for Marx’s contention here regarding the relationship between capital intensity and economic development;

Bergeaud, A., Cette, G. and Lecat, R. (2016) – processed by Our World in Data. “Capital Intensity (Bergeaud, Cette, and Lecat (2016))” [dataset].

↩ -

“The capitalist has his own views of this ultima Thule [the outermost limit], the necessary limit of the working day. As capitalist, he is only capital personified. His soul is the soul of capital. But capital has one single life impulse, the tendency to create value and surplus-value, to make its constant factor, the means of production, absorb the greatest possible amount of surplus labour. Capital is dead labour, that, vampire-like, only lives by sucking living labour, and lives the more, the more labour it sucks. The time during which the labourer works, is the time during which the capitalist consumes the labour-power he has purchased of him.” Marx, Karl. 1867. “Economic Manuscripts: Capital Vol. I - Chapter Ten.” Marxists.org. 1867. https://www.marxists.org/archive/marx/works/1867-c1/ch10.htm.

↩ -

Data from: Thomas, R and Dimsdale, N (2017) "A Millennium of UK Data", Bank of England OBRA dataset, http://www.bankofengland.co.uk/research/Pages/onebank/threecenturies.aspx ; Calculations by author.

↩ -

Thomas, R and Dimsdale, N (2017) "A Millennium of UK Data", Bank of England OBRA dataset, http://www.bankofengland.co.uk/research/Pages/onebank/threecenturies.aspx

↩ -

Nicolas Villarreal. 2023. “Artificial Intelligence, Universal Machines, and Killing Bourgeois Dreams.” Cosmonaut. May 11, 2023. https://cosmonautmag.com/2023/05/artificial-intelligence-universal-machines-and-killing-bourgeois-dreams/.

↩ -

Profit rates had negative YoY change just prior to 10 out of the last 14 recessions, and quickly drifted negative when the recession started in the other cases. “Rate of Profit Percent Change from Year Ago” | FRED | St. Louis Fed.” 2026. Stlouisfed.org. 2026. https://fred.stlouisfed.org/graph/?graph_id=1555067.

↩ -

Scharfenaker, Ellis, and Gregor Semieniuk. 2016. “A Statistical Equilibrium Approach to the Distribution of Profit Rates.” Metroeconomica 68 (3): 465–99. https://doi.org/10.1111/meca.12134.

↩ -

“(Total Deposits Held by the 90th to 99th Wealth Percentiles/Household Count in the 90th to 99th Wealth Percentiles)*1000000 | FRED | St. Louis Fed.” 2026. Stlouisfed.org. 2026. https://fred.stlouisfed.org/graph/?graph_id=1507415.

↩ -

U.S. Census Bureau, "Business Dynamics Statistics: Establishment Age by Establishment Size: 1978-2023," Economic Surveys, ECNSVY Business Dynamics Statistics, Table BDSEAGEESIZE, 2025, accessed on September 28, 2025, https://data.census.gov/table/BDSTIMESERIES.BDSEAGEESIZE?q=small+business&g=010XX00US. Additional calculations by author.

↩ -

States, United. 2026. “Explore Census Data.” Census.gov. 2026. https://data.census.gov/chart/BDSTIMESERIES.BDSEAGEESIZE?q=small+business&g=010XX00US&measure=FIRM&attrs=EMPSZES.

↩ -

Michał Kalecki. 2003. Theory of Economic Dynamics. London: Routledge. Pg 45-48

↩ -

“Let's go back to the beginning of the year. To keep the example as simple as possible, assume that all goods to be used over the year are bought at the beginning of the year (this is an expositional device only). Capitalists decide the level of production they would like for the current year.

They therefore buy a certain amount of producer goods, and hire a certain number of workers; the workers in turn use their wages to buy consumer goods. At the same time, capitalists also must buy a certain amount of consumer goods for their own personal consumption over the year. Notice that the effective demand originates entirely with the capitalist class: workers' wages are part of the year's gross investment expenditures by capitalists. It is quite illegitimate to treat consumption and investment as being functionally independent, since the bulk of consumption comes from wages, which are themselves a necessary aspect of invest ment expenditures. ' At the beginning of the year, therefore, it is the capitalist class through its consumption and investment expenditures which determines effec-tive demand. But who sells the commodities? Why, the capitalist class, of course!” ; Shaikh, Anwar. 1978. “An Introduction to the History of Crisis Theories.” U.S. Capitalism in Crisis, U.R.P.E. http://gesd.free.fr/shaikh78.pdf.

↩ -

For simplifying the math for these international statistics, I begin by composing the capitalist consumption share of income (CCSI) and convert this to a rate of capitalist consumption (CCRATE) with the following equation: CCRATE = CCSI/(1-CCSI). Or rather, that’s what I should have done, for some reason which escapes me now I decided to overcomplicate it by using CCRATE = CCSI + ((CCSI^2)/(1-CCSI)), which also equals CCSI/(1-CCSI).

↩ -

Data from: Thomas, R and Dimsdale, N (2017) "A Millennium of UK Data", Bank of England OBRA dataset, http://www.bankofengland.co.uk/research/Pages/onebank/threecenturies.aspx ; Calculations by author. ; “(1-(Gross Domestic Income: Compensation of Employees, Paid/Gross Domestic Product))+(Balance on Current Account, NIPAs-Gross Private Domestic Investment+(Federal Surplus or Deficit [-]/1000))/Gross Domestic Product | FRED | St. Louis Fed.” 2017. Stlouisfed.org. 2017. https://fred.stlouisfed.org/graph/?graph_id=1506291&rn=19.

↩ -

“(Gross Domestic Income: Net Operating Surplus: Private Enterprises-Taxes on Corporate Income, NIPAs-Balance on Current Account, NIPAs-Net Domestic Investment: Private-Rental Income of Persons with Capital Consumption Adjustment-GDI: Corp Profits with Inventory Valuation and CCAdj, Domestic Industries: Profits after Tax with Inventory Valuation and CCAdj: Undistributed Corp Profits with Inventory Valuation and CCAdj-Gross Domestic Income: Net Interest and Miscellaneous Payments+(Federal Surplus or Deficit [-]/1000))/(Gross Domestic Income: Compensation of Employees, Paid+Consumption of Fixed Capital) | FRED | St. Louis Fed.” 2017. Stlouisfed.org. 2017. https://fred.stlouisfed.org/graph/?graph_id=1509555&rn=181.

↩ -

For precision, rather than using the conversion formula from the capitalist consumption share of GDP, this uses the sum of depreciation and labor compensation for the denominator.

↩ -

“-Balance on Current Account, NIPAs/Gross Domestic Income: Net Operating Surplus: Private Enterprises | FRED | St. Louis Fed.” 2026. Stlouisfed.org. 2026. https://fred.stlouisfed.org/graph/?graph_id=1509701.

↩ -

“(Gross Domestic Income: Net Operating Surplus: Private Enterprises-Taxes on Corporate Income, NIPAs-Balance on Current Account, NIPAs-Net Domestic Investment: Private-GDI: Corp Profits with Inventory Valuation and CCAdj, Domestic Industries: Profits after Tax with Inventory Valuation and CCAdj: Undistributed Corp Profits with Inventory Valuation and CCAdj+(Federal Surplus or Deficit [-]/1000))/(Gross Domestic Income: Compensation of Employees, Paid+Consumption of Fixed Capital) | FRED | St. Louis Fed.” 2017. Stlouisfed.org. 2017. https://fred.stlouisfed.org/graph/?graph_id=1554899.; Graphic shows 67,000, the average US income, divided by the custom Fred data series linked here, with the World War 2 years excluded due to near and below zero values caused by high government deficits producing non-linear effects.

↩ -

Villarreal, Nicolas D. 2023a. “The Stealth Bank Bailout.” Substack.com. Pre-History of an Encounter. September 2, 2023. https://nicolasdvillarreal.substack.com/p/the-stealth-bank-bailout.

↩ -

Schularick, Moritz. 2014. “Public and Private Debt: The Historical Record (1870–2010).” German Economic Review 15 (1): 191–207. https://doi.org/10.1111/geer.12031.

↩ -

Tian, Lihui, and Saul Estrin. 2007. “Debt Financing, Soft Budget Constraints, and Government Ownership Evidence from China.” The Economics of Transition 15 (3): 461–81. https://doi.org/10.1111/j.1468-0351.2007.00292.x

↩ -

Opferkuch, Beulah Chelva; Van Der Does De Willebois, Emile Johannes Marie; Jenkinson, Nigel Harrison; Menezes, Antonia Preciosa; Muro, Sergio Ariel; Rouillon, Adolfo; O'Reilly Gurhy, Bryan; Søren Lejsgaard Autrup.

Addressing the Corporate Debt Overhang (English). Equitable Growth, Finance and Institutions Insight Washington, D.C. : World Bank Group. http://documents.worldbank.org/curated/en/099015006232222104

↩ -

Occhino, Filippo. 2010. “Is Debt Overhang Causing Firms to Underinvest?” Economic Commentary, no. 2010-07 (July). https://www.clevelandfed.org/publications/economic-commentary/2010/ec-201007-is-debt-overhang-causing-firms-to-underinvest.

↩ -

“Capitalist Consumption Measures.” n.d. FRED, Federal Reserve Bank of St. Louis. https://fred.stlouisfed.org/graph/?graph_id=1509631.

↩ -

Data from: Feenstra, Robert C., Robert Inklaar and Marcel P. Timmer (2015), "The Next Generation of the Penn World Table" American Economic Review, 105(10), 3150-3182, available for download at www.ggdc.net/pwt ; Calculations by author.

↩ -

Villarreal, Nicolas. 2025. “The Chinese Encounter.” Substack.com. Pre-History of an Encounter. October 15, 2025. https://nicolasdvillarreal.substack.com/p/the-chinese-encounter.

↩ -

“World Bank Open Data.” World Bank Open Data, 2024, data.worldbank.org/indicator/NE.RSB.GNFS.ZS?view=map. Accessed 15 Oct. 2025.;

“Central Government Debt, Total (% of GDP) | Data.” Data.worldbank.org, data.worldbank.org/indicator/GC.DOD.TOTL.GD.ZS.

↩ -

“China is a big victim of Chinese overinvestment! Latest Penn World Tables show that by 2023 Chinese capital efficiency below even Japan's, and far below the US level, despite still being much poorer than either.” Bird, Mike. 2025. X (Formerly Twitter). December 23, 2025. https://x.com/i/status/2003531133586407496.

↩ -

“Transcript: China’s Economy vs the World. With Michael Pettis.” @FinancialTimes, Financial Times, 24 Sept. 2025, www.ft.com/content/10cee454-d4c0-4421-9b64-e73684bbb27f. Accessed 15 Oct. 2025.

↩ -

Scharfenaker, Ellis, and Gregor Semieniuk. 2016. “A Statistical Equilibrium Approach to the Distribution of Profit Rates.” Metroeconomica 68 (3): 465–99. https://doi.org/10.1111/meca.12134.

↩ -

Organization for Economic Co-operation and Development. 1957. “Total Share Prices for All Shares for the United States.” FRED, Federal Reserve Bank of St. Louis. January 1, 1957. https://fred.stlouisfed.org/series/SPASTT01USM661N.

↩ -

“Yearbook.” 2022. National Venture Capital Association (NVCA). https://nvca.org/wp-content/uploads/2022/03/NVCA-2022-Yearbook-Final.pdf. Pg 12.

↩ -

Ibid., Pg 28

↩ -

Lichtenberg, Nick. 2025. “Without Data Centers, GDP Growth Was 0.1% in the First Half of 2025, Harvard Economist Says.” Fortune. October 7, 2025. https://fortune.com/2025/10/07/data-centers-gdp-growth-zero-first-half-2025-jason-furman-harvard-economist/.

↩ -

“As of end-June, loans to the manufacturing sector were up by 12.99 percent from the previous year-end, while loans to strategic emerging industries surged by 22.92 percent, with technology finance loans outpacing industry peers, Zhang noted. Since early 2025, banks have sharply increased lending to sectors linked to new quality productive forces. As of June 2025, ICBC's technology loans climbed to 6 trillion yuan, up more than 1 trillion yuan from the year's start.” A 13% rise in manufacturing lending in a time when inflation was essentially zero. Compare this situation to that of the U.S., where financing for manufacturing fell in real year over year terms by 14% in 2024, and saw a precipitous decline the past 25 years. ; Tong, Ma. 2025. “Total Loan of Listed Banks Exceeds $25 Trillion by End-June - Global Times.” Globaltimes.cn. 2025. https://www.globaltimes.cn/page/202509/1342445.shtml. ; “Quarterly Financial Report: U.S. Corporations: All Manufacturing: Short-Term Debt, Original Maturity of 1 Year or Less: Loans from Banks/Consumer Price Index for All Urban Consumers: All Items in U.S. City Average | FRED | St. Louis Fed.” 2026b. Stlouisfed.org. 2026. https://fred.stlouisfed.org/graph/?graph_id=1554908.

↩ -

See the decline from 5.5% to 4% starting in April, Trump’s infamous “Liberation Day”. ; Federal Reserve Bank of St. Louis. 2019. “Personal Saving Rate.” Stlouisfed.org. 2019. https://fred.stlouisfed.org/series/PSAVERT.

↩ -

Cottrell, Allin F, Paul Cockshott, Gregory John Michaelson, Ian P Wright, and Victor Yakovenko. 2009. Classical Econophysics. Routledge. Pg 263-280

↩