In their recent article Energy, Ecology, and the 'Transition': Why Logistics is a Class Question Foppe de Haan suggests that talk of an energy “transition” is a sort of bourgeois ideology, as the recent rise of renewable power sources, most notably solar, will only ever be additive within capitalism and never actually displace fossil fuels.

Here is one passage that encapsulates the argument:

Even where LCOE is accurate, lower cost does not translate into higher profit in unbundled electricity markets, because competition, the cannibalization effect (rising renewable energy (RE) penetration depressing the wholesale prices from which RE earns revenue), and revenue uncertainty make profitability unknowable in advance. JPMorgan's head of energy strategy calls LCOE "a practical irrelevance" for the financiers who actually decide whether projects proceed. Typical RE project returns are 5–8%, against 15%+ for oil and gas — which is why no major RE build-out anywhere has proceeded without state guarantees.

There are a few contradictions here, the most important of which are if renewable energy is putting downward pressure on wholesale prices that will also negatively impact oil and gas project returns. Past oil and gas returns will not be indicative of oil and gas returns in a world with greater renewable energy penetration.

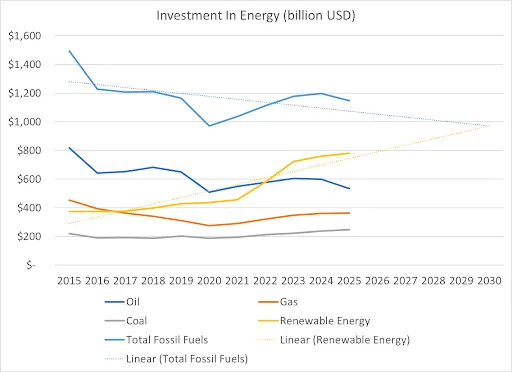

And indeed, despite all the legacy of decades of fossil fuel investment, things are changing. We can look at investment trends empirically and see that total fossil fuel investment has been falling since the 2010s shale boom, while renewable energy investment has been rising, with renewables expected to exceed all fossil fuel investment in 2030 with some naive linear extrapolation.[1] Indeed, renewable energy already in 2025 exceeded every individual type of fossil fuel investment, including oil, gas, and coal.

Of course, fossil fuel investment will need to fall much further in order to matter, as the capital stock has been built up for decades and will take further decades to naturally depreciate away, assuming it is not destroyed in war or forced to be shuttered by governments. But it’s worth noting here that the linearity of this extrapolation is almost certainly an overestimate of the sticking power of fossil fuels. The price decline in solar panels and batteries has been non-linear in nature,[2] and so has their adoption.[3] The energy crisis caused by the Iran war will no doubt also generate more demand from states and businesses.

One thing that was left unremarked by Haan was the role that energy consumers, whether businesses or households, would play in the future of energy markets. Some of the largest recent purchasers of Chinese solar have, after all, been not for grid projects, but rooftop solar in places like Pakistan and other developing countries, where grid power has been unreliable. But for any consumer of energy, whether in rich or poor countries, solar represents a unique cost-saving proposition that will eventually pay for the upfront capital expended. This is why the price does matter, whether or not grids are capable of absorbing the vicissitudes of solar energy production.

The creation of cheap solar via incredibly high Chinese investment and sustained industrial policy cannot be understated here. For the first time, the majority of the developing world may be freed from onerous interdependency and compelled dollar-denominated exports to secure energy. The catastrophe in Cuba could have been largely averted if investment in solar had begun much earlier, as would the catastrophe facing much of the developing world due to the ongoing energy crisis. The industrial and natural resource costs of solar are, in fact, fundamentally different from the costs of fossil fuels, for the simple reason that fossil fuels are a fuel while solar is a piece of fixed capital. Solar panel consumption occurs only at the pace of their depreciation, whereas fossil fuels have to be consumed continuously in order to create energy. This means that while the natural resource costs of transitioning to solar energy may be comparable to those of fossil fuels upfront, they will necessarily decline dramatically once the capital stock stabilizes. And as R&D knowledge accumulates, we should expect to see many of the more exotic materials required in solar panel and battery supply chains replaced by more common ones.

Haan brings up that capitalism flourishes based on the costs associated with investment. This is certainly true, as it is true that in capitalism, it is only the flows of consumption that generate income, rather than stocks of wealth. But it is not true that, for this reason, capitalists or consumers or states (with perhaps the exception of the United States of America) will prop up fossil fuel infrastructure to maintain high levels of expenditures. I’ve heard a similar argument from Malcom Harris that this is the logic behind the AI data center buildout. But both the AI data centers and the fossil fuel investment in the US are major exceptions to the trends of US investment overall. When Haan says that investment in fossil fuel infrastructure was 2/3rds of net investment in industry for the US between 2009 and 2019, this has less to do with the strength of the fossil fuel industry and more to do with the weakness of industrial investment in the US, which has ceased to grow as a share of GDP since the beginning of neoliberalism.[4] Both the oil and data center booms were/are largely failed attempts at rent capture, specifically natural resource and land rents for the oil boom, and software IP rents for the AI boom. If it were true that capitalists would make fixed capital expenditures simply for the sake of economic activity, neoliberalism would not have the character of massive deindustrialization.

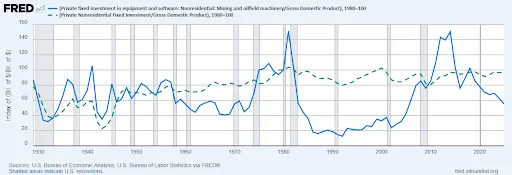

Financial investors in the oil and gas sector in the US were not particularly rewarded by their enthusiastic fixed capital investments, seeing essentially flat returns for a decade up until the recent energy crisis. This is one reason why American oil companies are not particularly interested in putting money towards boosting output now, despite the President’s pleas and a massive price spike: a Fed survey of oil executives in April put the increase in oil output for 2026 and 2027 as between 0 and 2%.[5] Indeed, if the UAE can survive the war with its oil infrastructure intact, its exit from OPEC would likely mean the forced closure of American marginal producers.

For what it’s worth, we’ve also seen recent jitters from the stock market as the huge fixed capital investments have begun cutting into the free cash flow of major tech companies, the sort of things which would have been put towards stock buybacks and dividends in years past. The more that’s actually invested in production, after all, the less the capitalist class can actually consume at any given moment.

Certainly, the capitalists who own fossil fuel infrastructure will be reluctant to retire it, and will be seeking to keep them operational even if they receive a lower than average rate of return as this will likely be higher than the return from scrapping the project. But for businesses planning out their own investments, and households looking at how to minimize their expenses, there will be little sympathy. Anyone who has the money to make the upfront investment in solar and batteries will do so given the right price. In the US, this price is artificially inflated by trade barriers with China, making it some 2 to 4 times more expensive to install rooftop solar than elsewhere. Grid scale batteries will further smooth out night vs day pricing, and whether or not states and grid operators make the specific decision to switch to renewables, fossil fuel plants will increasingly be competing with each other for the few stretches of cloudy weather.

Will this mean that capitalism can save us from climate catastrophe? Though I would never totally discount the ability for bourgeois society to squirm its way out of another predicament, I doubt it. It really does depend on the “how fast” question which Haan dismisses as symptomatic of the bourgeois ideology of transition. All I claim is that in fact there will be a transition. Here, the writing is on the wall. The dramatic decline in solar panel prices, the effects of the energy crisis, the non-linear adoption and the overall rise in renewable investment and decline in fossil fuel investment, these things all point in the same direction. Citing the recent book “More and More and More” with the same thesis, Haan asserts that energy transitions have never happened and indeed are generally impossible:

This framing is wrong — and wrong in a way that the historical record makes clear. Fressoz demonstrates that there has never been an energy transition in the substitution sense. Every new energy source has added to rather than replaced its predecessors: global coal consumption is higher today than at any point in history; the world burns three times more wood than a century ago; oil consumption continues to rise. The reason is not institutional inertia alone but material symbiosis: each energy source depends on the others, both as energy inputs and as material inputs to its infrastructure. Oil infrastructure requires coal-fired steel (pipelines, rigs, refineries, engines — each tonne of inter-war oil generated 2.5 tonnes of induced coal consumption). Coal and mineral ores are mined with diesel-fuelled machinery and moved by trains and ships. Wood extraction now requires oil (chainsaws, roads, fertilizers for industrial plantations). And 'renewable' solar panels and wind turbines require all of the above: steel towers, copper wiring, concrete foundations, coking coal, and the entire fossil-powered mining and refining chain. A 'transition' that sees fossil fuels decline in relative terms but stagnate in absolute consumption solves little if our aim is decarbonization.

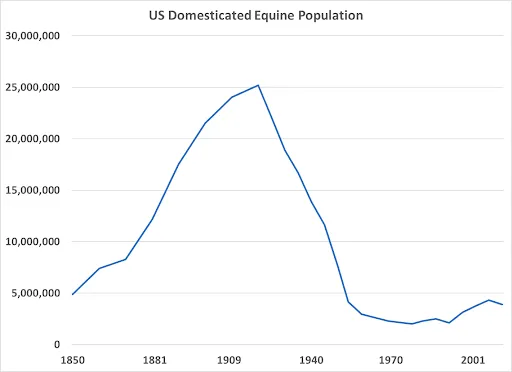

At the beginning of his article, however, Haan notes that the exosomatic energy, the energy outside of the body repurposed towards a particular end, includes things such as a draught horse. Here, indeed we can speak of an energy transition.

As you can see, the US domesticated equine population is currently a fraction of what it once was during the times when horsepower was an essential industrial energy.[6] Certainly, whatever material symbiosis, (glue and gelatin for example), or institutional inertia horsepower had was not enough for it to be replaced by coal and gas.

Haan and Fressoz also fail to think through the other side of this coin, that as oil and gas become less in demand, so too will their byproducts become more scarce and costly, and the synergy these things once provided will evaporate. Technology change also makes these particular input-output relationships redundant over time. Electrification has gone apace in many industrial and consumer settings which were once dominated by direct fossil fuel consumption, such as lawn mowers, metal foundries, cars, kilns and so on. As much as the energy and supply chain crisis created by the Iran War is exposing our dependency on fossil fuels, it also shows the extent to which many products are effectively subsidized by being byproducts of fossil fuel extraction. The lower the demand for fossil fuels as people switch to cheaper solar energy will thereby result in searching for solar-electrical alternatives (both in process of production or products themselves), whether in fertilizer or aluminum or plastics.

Certainly, the capitalist tendency towards avoiding fixed capital investment perhaps could have prevented a transition if only huge investments were possible to deploy any quantity of renewables. This is a major problem for wind energy, which is highly dependent on interest rates for the success or failure of any project. But solar being so much easier to deploy, and at any arbitrary quantity, gets around this issue. Indeed, anyone who can afford a smartphone today can almost certainly afford a solar panel and battery pack, which is perhaps the majority of the planet’s population.

The achievement of China in this respect, despite the material and human costs, is immense. It comes down not just to the technical achievements of workers and engineers, but also the incredibly high investment rate in China and of its working class households. China, unlike the US and most capitalist nations, actually consumes less than its total wage bill, an economic feature which breaks the classical Marxist doctrine of wages being set by the costs of the reproduction of the working class. The revolutionizing of the productive forces which enables the solar energy transition must therefore be considered a chief achievement of the proto-socialist elements of the Chinese economy, as a sacrifice of its proletariat and an economic plan under state capitalism orchestrated by the Chinese Communist Party. This is not to erase the suffering of those children mining for raw materials in Africa or slave Uyghur labor involved in these supply chains but to state a fact.

The policy of the socialist left in the west should be to continue to criticize these crimes and indignities facing workers, while also seeking a path to eliminate trade barriers to these essential clean energy industries given that these issues are addressed by suppliers, as well as pushing for more domestic investment in these industries to accelerate the energy transition. Perhaps that is a cliche answer, but, as they say, cliches occur precisely because everyone desires them.

Liked it? Take a second to support Cosmonaut on Patreon! At Cosmonaut Magazine we strive to create a culture of open debate and discussion. Please write to us at submissions@cosmonautmag.com if you have any criticism or commentary you would like to have published in our letters section.

-

IEA (2025), Global investment in clean energy and fossil fuels, 2015-2025, IEA, Paris https://www.iea.org/data-and-statistics/charts/global-investment-in-clean-energy-and-fossil-fuels-2015-2025, Licence: CC BY 4.0

↩ -

IRENA (2025); Nemet (2009); Farmer and Lafond (2016) – with major processing by Our World in Data. “Solar photovoltaic module price” [dataset]. IRENA, “Renewable Power Generation Costs in 2024”; Nemet, “Interim monitoring of cost dynamics for publicly supported energy technologies”; Farmer and Lafond, “How predictable is technological progress?” [original data]. Retrieved May 17, 2026 from https://archive.ourworldindata.org/20260507-171259/grapher/solar-pv-prices.html (archived on May 7, 2026).

↩ -

Ember (2026); Energy Institute - Statistical Review of World Energy (2025) – with major processing by Our World in Data. “Share of electricity generated by coal” [dataset]. Ember, “Yearly Electricity Data Europe”; Ember, “Yearly Electricity Data”; Energy Institute, “Statistical Review of World Energy” [original data].

↩ -

“Private Fixed Investment in Equipment and Software: Nonresidential: Mining and Oilfield Machinery/Gross Domestic Product | FRED | St. Louis Fed.” Stlouisfed.org, 2017, fred.stlouisfed.org/graph/?graph_id=1596673. Accessed 18 May 2026.

↩ -

Findlay, Stephanie. “US Shale Bosses Resist Boosting Oil Output over Iran War “Chaos.”” @FinancialTimes, Financial Times, 23 Apr. 2026, www.ft.com/content/273c0321-0678-4ac0-9ccc-432301865b4c?syn-25a6b1a6=1. Accessed 18 May 2026.

↩ -

“USDA Horse Total, 1850-2012 | Data Paddock.” Data Paddock, 11 Aug. 2019, datapaddock.com/usda-horse-total-1850-2012/.

↩