The recent article by Nicolas D Villarreal on “The Capitalist in the 21st Century” has a wealth of useful analysis, and I appreciated particularly its use of figures to punch holes in some common misinterpretations of Marx, including its treatment of unemployment and the declining rate of profit.

However, the article suggests an alternative causal explanation of the evident slowdown in capitalist growth and innovation in the past period, and there I think finds itself on shakier ground. It essentially posits that capitalist investment (and hence economic development) is limited by high capitalist consumption. However, there is no reason to believe this is the case. Historically, and under Marx’s analysis, the limiting factor to capitalist production is not the consumption of capitalists, but their ability to profit from investment. This is to say that new investment will only take place not when it is profitable, but when it meets or exceeds the average rate of profit. When the capitalist is unable to invest in such a way, they simply do not invest at all. We witness similar phenomena all the time, for example when a commercial storefront lies unoccupied because the landlord is unwilling to rent at below market rate.

As an accounting identity, Villarreal calculates capitalist consumption as profit less gross investment. But this has a flaw. Profit may go into investment, it may go into consumption, or it may, in effect go under a mattress. This is to say that it may go into savings or speculation. Savings in banks, in turn, will only show up again in GDP if it is then used in investment. But a large portion is not.

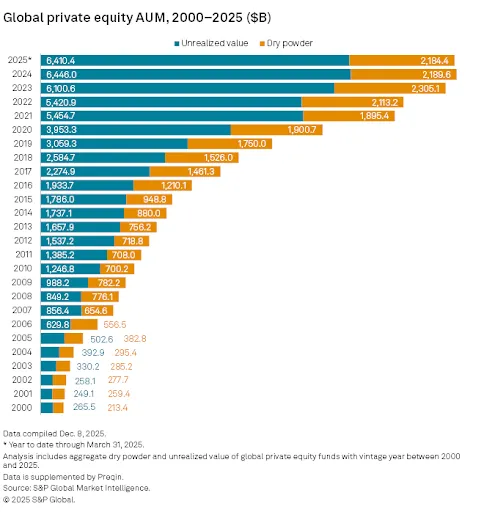

While we don’t have direct measures of how much “uninvested but ready” capital exists, there are areas where we do. For example, private equity firms report both assets under management and cash at hand – the latter referred to as “dry powder”. There is currently over two trillion in private equity dry powder alone[1]:

Similarly, large enough capitalist firms are effectively also banks, because of the amount of capital they manage beyond their direct expenditure in their own development. Apple currently has about 66 billion cash on hand, and Google 126 billion.[2] We could repeat the same exercise for every major firm, as well as banks, hedge funds, venture capital, and a variety of other institutions, and would doubtless arrive at a number of many trillions, perhaps even similar to the US GDP itself. If there were sufficiently profitable ways to invest this cash, we can be assured that this reserve (which Marx termed a “hoard”) would be invested. To be sure, in Marx’s models of capitalist reproduction, he pointed out both the necessity and instability of some form of hoard, to accumulate funds for sporadic repairs of machinery, or new large outlays, etc. But there’s no necessary balancing force that will inevitably cause a hoard to be spent down in proportion to its growth, and in fact disproportion of the hoard is both symptomatic of and casual to capitalist crises. Various policy attempts to set capital reserves in renewed motion (not attempts to reduce capitalist consumption) were core to policy responses to the Great Financial Crisis – and at the time capital reserves were substantially lower than they are today.

Furthermore, the answer to the problems induced by the necessity of a hoard is its “socialization” into a common fund via the development of finance. And so we see finance is not opposed to industrial development but its necessary handmaiden, and in allowing the better management of capital reserves on a day-to-day basis nonetheless lays the way for greater and more complex “general” crises that strike the system as a whole as the web of financial entanglements transmits contagion across sectors and national boundaries.

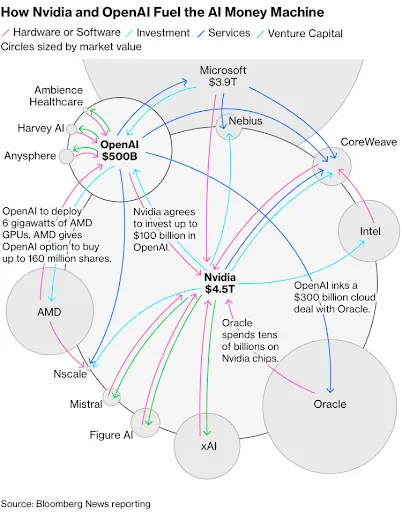

Indeed, in the modern economy, a lack of cash-on-hand (which we have seen is not the case here) does not prevent investment even if it were to occur. A “hot” economy generates monetary velocity and speculation (proto-bubble phenomena) to allow investment even absent cash reserves. For example, the AI sector is currently very hot. But many investors are wisely not pouring all their spare reserves into it. So where does the funding come from? It comes from the infamous circular financing scheme where burgeoning speculative asset appreciation allows some firms such as Nvidia to essentially lend their speculative valuation to their customers, whose valuations then in turn increase, allowing them to borrow against such and keep the whole asset bubble afloat[3]:

Similar phenomena have occurred throughout history. Whensoever there is a gold rush, capital, scarce though it may have appeared beforehand, will manifest as though apported through a séance.

Villarreal correctly points to an overall increase in productivity that comes from funding negative profit rate investments that create infrastructure to bolster the economy as a whole. However, we need not locate the difference between the U.S. and China in this regard as fundamentally about the relative consumption rate. Rather, China has a significant core of state-owned industry and investment, and a government which is not ruled by a capitalist class in the interests of their individual profits. This is to say that despite the presence of capitalist investment and firms in China, it is not a capitalist state. It is this difference that accounts for the productivity of the Chinese economy – not curtailed capitalist consumption, but state control and management that support general development at the expense of individual capitalist profit.

Liked it? Take a second to support Cosmonaut on Patreon! At Cosmonaut Magazine we strive to create a culture of open debate and discussion. Please write to us at submissions@cosmonautmag.com if you have any criticism or commentary you would like to have published in our letters section.